Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

Banks in United Kingdom, Germany, France, Spain and Italy are under big pressure after U.S. authorities’ actions to stem a possible cascade of runs following the collapse of Silicon Valley Bank (SVB). The STOXX Europe 600 Banks Index is down around 7% over the past five days.

But the decline only takes major European lenders’ shares back to their January levels. They’re priced for lower earnings, but not a crisis.

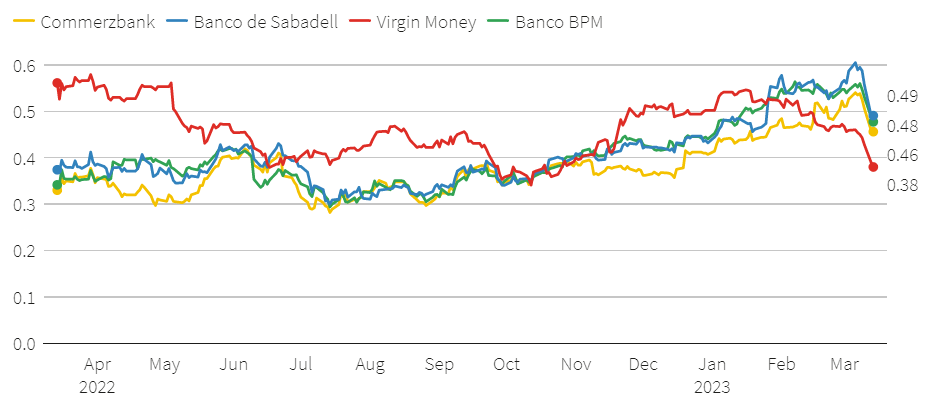

The recent market slump seems dramatic. Smaller or historically low-returning banks like Commerzbank, Banco de Sabadell, Virgin Money and Banco BPM have suffered the most.

The worst-case scenario would be if customers with uninsured deposits at smaller European lenders pulled their money, spooked by last week’s rapid failure of SVB.

But that’s not what investors are betting on. Even after the share-price dip, those four lenders still have higher valuations than they did in October, using multiples of 2023 tangible book value gathered by Refinitiv Datastream.

None of them are particularly highly valued, admittedly, but nor are they priced for a bank run. Charlie Nunn, the boss of Lloyds Banking Group, said on Tuesday that he is not yet seeing an incoming rush of deposits from smaller lenders, which should help ease concerns.

The cost of insuring European banks’ debt against a default, another popular fear gauge, has risen but not by much – other than for stricken wealth manager Credit Suisse.

Investors’ relative calm makes sense. SVB’s problems were caused by a toxic combination of under-water fixed-income assets alongside flighty deposits.

As the liabilities disappeared, it had to realise losses on the securities. European balance sheets look very different. Debt securities are 12% of euro area lenders’ assets, according to Moody’s, compared with 30% for the United States.

Deposits have grown relatively slowly in Europe, suggesting they may be less volatile, while the Europeans also generally have more cash on reserve at the central bank, the rating agency said.

The upshot is that European lenders should be less exposed to a run, and would in any case be better placed to handle one.

The selloff, then, probably has more to do with investors resetting their rate-hike expectations. Central bankers may be less willing to tighten monetary policy given the recent chaos, meaning a hoped-for windfall for the banking sector may be smaller than expected.

Far from a crisis, European lenders may have just fallen back to where they were a few months ago.

Multiple of share price to 2023 tangible book value per share, using analysts’ estimates, for selected mid-sized European banks. Note: Share price divided by 12-month forward tangible book value per share. Liam Proud | Reuters Breakingviews. Source: Refinitiv Datastream