Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

Whereas prices of some commodities are retreating from recent peaks, the EU economy remains vulnerable to developments in energy markets due to its high reliance on Russian fossil fuels.

With gas prices nearing all-time highs energy inflation is on the rise. Food inflation is also surging, but pressures are broadening further as higher energy costs are passed-through to services and other goods.

Lower income households are especially hit by the protracted rise in prices. Whereas businesses still eye an expansion of economic activity, they are less optimistic about the future, which will weigh on investment.

Households are just as negative about the future as they were at the onset of the pandemic, which is set to drag on the recovery of private consumption.

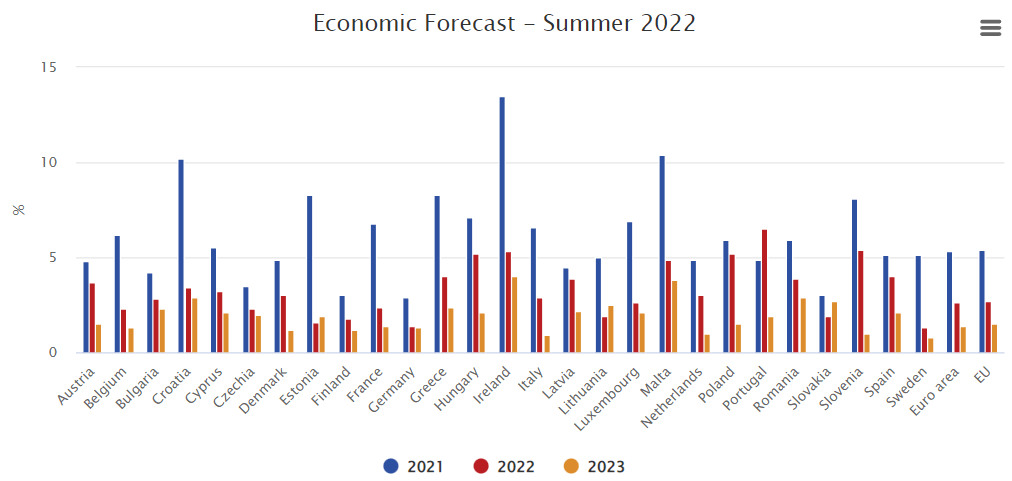

Overall, real GDP is forecast to grow by 2.7% in 2022 and 1.5% in 2023 in the EU and by 2.6% in 2022 and 1.4% in 2023 the euro area.

The projected annual growth rate for this year is propped up by the momentum gathered with the recovery of last year and a stronger first quarter than previously estimated.

Both bring acquired growth at the first quarter of this year to a solid 2.7% for the EU and 2.4% for the euro area. Economic activity is expected to have weakened in the second quarter, but should regain some traction during summer, thanks to a promising tourism season.

In 2023, economic growth is expected to gather some momentum, on the back of a resilient labour market, moderating inflation, support from the Recovery and Resilience Facility and a still large amount of excess savings. However, on an annual basis there is a downward revision of almost one percentage point compared to the Spring Forecast.

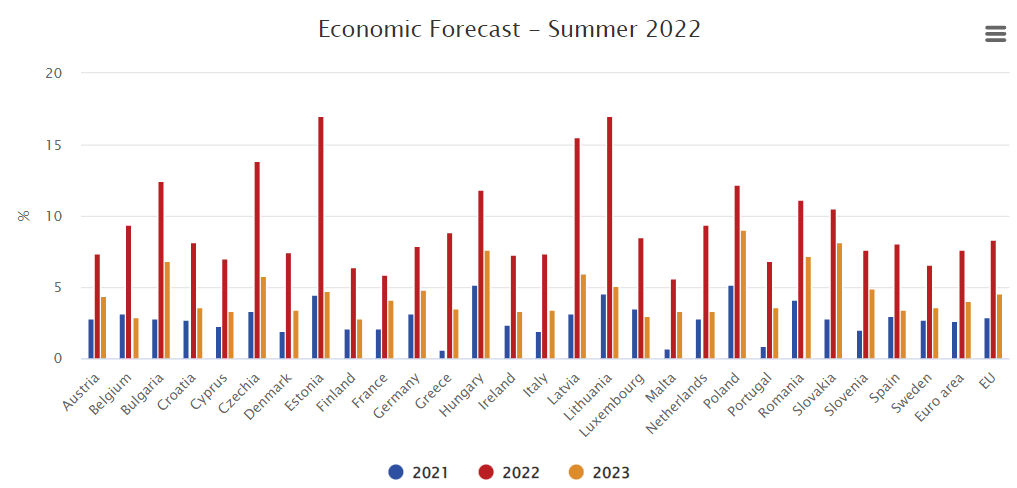

Inflation in the euro area is projected to peak at a new record high of 8.4% in the third quarter of 2022. As the pressures from energy prices and supply constraints fade, inflation is expected to decline steadily thereafter and to fall below 3% by the end of 2023. The annual rates of 7.6% in 2022 (8.3% in the EU) and 4.0% in 2023 (4.6% in the EU) imply upward revisions by more than one percentage point from the Spring Forecast.

Risks to the forecast for economic activity and inflation are heavily dependent on the evolution of the war. Further increases of gas prices could strengthen the stagflationary forces currently at play. Second round effects could amplify these forces and lead to a sharper tightening of financial conditions that would not only weigh on growth, but also on financial stability.

At the same time, recent downward tendencies of oil and other commodities’ prices could intensify, bringing about a faster deceleration in inflation. Moreover, private consumption could prove more resilient to increasing prices if households were to use more of their savings. Finally, COVID-19 remains a risk factor.