Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

August saw a second successive monthly reduction in business activity across the euro area, according to early PMI survey indicators, amid a further decline in new orders.

Cost of living pressures sapped demand in the service sector, leaving activity only just inside growth territory, while manufacturing remained in a downturn midway through the third quarter of the year.

Although remaining elevated, there were again signs that inflationary pressures at businesses have passed their peak, with rates of increase in both input costs and output prices softening across the board.

Concerns over the economic outlook meant that business confidence remained muted in August. This relatively weak sentiment, plus a sustained downturn in customer demand, meant that firms were increasingly reticent to expand staffing levels and the rate of job creation softened to the slowest in almost a year-and-a-half as a result.

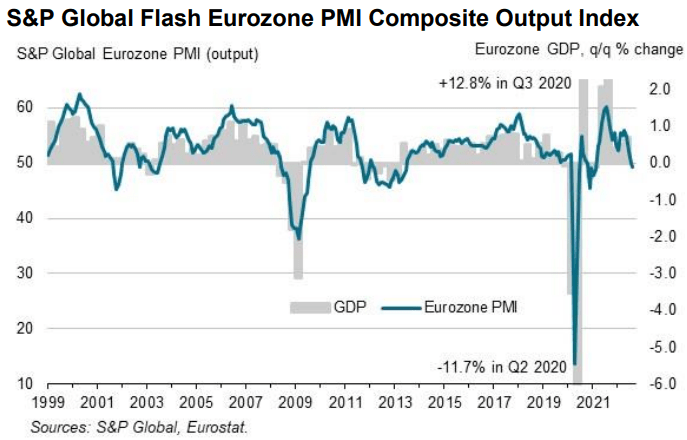

The seasonally adjusted Eurozone PMI Composite Output Index dropped to 49.2 in August, from 49.9 in July, according to the ‘flash’ reading.

The index signalled a second successive reduction in business activity across the eurozone following a 16-month period of growth. Although still only slight, the latest decline was sharper than that seen in July.

The overall drop in output was again driven by a contraction in the manufacturing sector, where production fell for the third month running and at a solid pace.

That said, the service sector barely registered any improvement in activity during August as the rate of expansion slowed for the fourth consecutive month to the softest since the sector returned to growth in April 2021.

The overall reduction in business activity in the euro area was mainly centred on the largest national economies. Germany posted the sharpest decline in output since June 2020 as manufacturing production continued to fall markedly and the contraction in services activity

accelerated.

Activity in France decreased for the first time in a year-and-a-half, reflective of a sharp drop in manufacturing output and softer growth of services activity. Outside of the ‘big-two’, output continued to increase, albeit only marginally.

Particularly sharp declines in output were seen across basic materials categories and in the autos sector, but reductions were also recorded in parts of the service sector, including in tourism & recreation and real estate.

Business activity was undermined by declining demand as new orders fell solidly for the second month running. New business was down in both the manufacturing and service sectors, with the former continuing to post the sharper contraction.

The steep drop off in demand in the manufacturing sector has seen a build-up in unsold goods as firms have found it difficult to shift finished products.

Post-production inventories increased at the sharpest pace in more than 25 years of data collection in August, with the rate of accumulation hitting a record high for the second month in a row.

Strong inflationary pressures were again key to the reduction in new orders, with both input costs and output prices continuing to rise rapidly.

That said, rates of inflation at businesses slowed again over the month. Input costs increased at the softest pace in close to a year, while output charge inflation was the weakest in the year-to-date.

Softer inflationary pressures were recorded across both the manufacturing and service sectors. Alongside signs of inflation at companies waning, there was further evidence that constraints in manufacturing supply chains eased in August.

Suppliers’ delivery times continued to lengthen markedly, but to the least extent since October 2020. Although improving slightly from July, confidence in the year-ahead outlook for activity remained relatively muted amid worries of an economic downturn.

Sentiment was the second-lowest since the initial wave of the COVID-19 pandemic. This muted confidence, alongside falling new orders and a lack of pressure on capacity (backlogs of work decreased for a second successive month), meant that firms moderated their hiring activities.

Employment increased for the nineteenth month running as some companies continued to make efforts to rebuild workforces following

the pandemic, but the rate of job creation eased for the third month in a row to the softest since March 2021.

Rates of growth eased to 17-month lows in Germany and the ‘rest of the eurozone’, with France seeing the softest expansion in 13 months.