Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

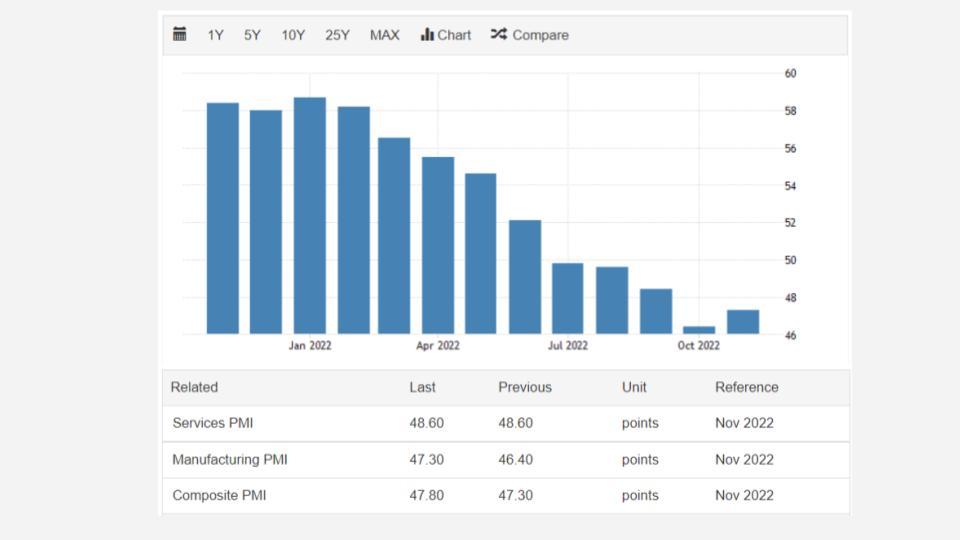

The seasonally adjusted Eurozone PMI Composite Output Index rose from 47.3 in October to 47.8 in November, according to the preliminary ‘flash’ reading based on approximately 85% of usual survey responses.

The PMI has now registered below the neutral 50.0 level, indicating falling business activity levels, for five consecutive months, albeit with the latest data signalling a moderation in the rate of contraction.

Nevertheless, the PMI data for the fourth quarter so far put the eurozone economy on course for its steepest quarterly contraction since late-2012, excluding pandemic lockdown months.

Manufacturing continued to lead the downturn, with factory output dropping for a sixth successive month. Although the rate of production decline eased, the latest fall was still the second-strongest recorded over the past decade if the height of the pandemic is excluded. Service sector output also fell, down for a fourth consecutive month, contracting at an unchanged rate compared to October.

However, such a rate of decline had not been witnessed outside of pandemic lockdowns since June 2013. Within the euro area, Germany again reported the steepest downturn, the composite PMI at 46.4 to register a fifth monthly drop in output in as many months.

Although the latest decline was the weakest since August, it was still the third largest since 2009 barring pandemic lockdowns. While Germany’s manufacturing and service sectors both suffered similarly steep rates of contraction, the former saw a marked cooling in the rate of decline.

Output meanwhile fell in France, the composite PMI registering 48.8 to signal the first drop in business activity since February 2021. Service sector output contracted for the first time since March 2021 and manufacturing output fell for a sixth straight month, albeit the rate of decline moderating to the slowest since August.

Output fell in the rest of the eurozone for a third month in a row, albeit with November’s decline being the smallest seen over this sequence. A marginal return to growth in the service sector contrasted with a steepening fall in factory production, which fell at a rate not seen since March 2013 barring pandemic lockdown months.

By sector, any growth was confined to industrial and software services, media and pharmaceuticals & biotech firms. The steepest downturn was again seen in chemical & plastics, with notably steep declines also recorded for basic resources (linked in part to high energy costs).

Especially marked falls also continued to be seen for real estate, transportation, tourism & recreation and autos. New orders for goods and services meanwhile fell for a fifth month running to signal a further marked drop in demand.

Although the rate of loss eased from October, the drop in orders was the second-largest seen in the past two years. While new orders fell at a reduced rate in manufacturing, the rate of loss intensified slightly in services.

The drop in new orders meant companies were again reliant on existing backlogs of work to help maintain business activity levels, causing backlogs of orders to fall for a fifth consecutive month, dropping at the sharpest rate for two years.

A particularly sharp decline was again recorded in manufacturing, but backlogs of work also showed a renewed decline in services. The deteriorating order book situation led to a growing reluctance to add to workforce numbers, resulting in the smallest monthly increase in employment since March 2021.

The hiring slowdown was led by the service sector, though factory payroll growth also remained subdued. By country, jobs growth picked up in Germany but deteriorated in France.

One positive consequence of weaker demand was a marked reduction in supply chain delays as input buying fell sharply again. Average supplier delivery times faced by eurozone factories lengthened to the least extent since August 2020.

Factories in Germany even reported the first improvement in supplier performance since July 2020. In addition to facilitating higher production in some cases, the improving supply situation – combined with weakened demand – took further pressure off prices.

Average input prices paid by manufacturers rose at a markedly reduced rate as a result, showing the smallest monthly gain since December 2020.

Service sector input cost inflation also moderated, down to the second-lowest in the past nine months. Measured across both sectors, input cost inflation cooled to the lowest since September 2021, albeit remaining elevated by historical standards thanks principally to high energy costs.

Average prices charged for goods and services also rose at a reduced rate, albeit likewise continuing to climb sharply, the rate of inflation cooling for a second month in a row to register the smallest increase since August.

Rates of selling price inflation eased in both manufacturing and services, most notably to a 20-month low in the former. Finally, business expectations for the year ahead remained subdued, improving slightly for a second successive month but still running at the third-lowest since the early pandemic lockdowns.

Confidence continued to be stymied by concerns over the growth outlook, the rising cost of living and the energy crisis, in turn linked to the Ukraine war, as well as rising interest rates.

Press release can be found here.