Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

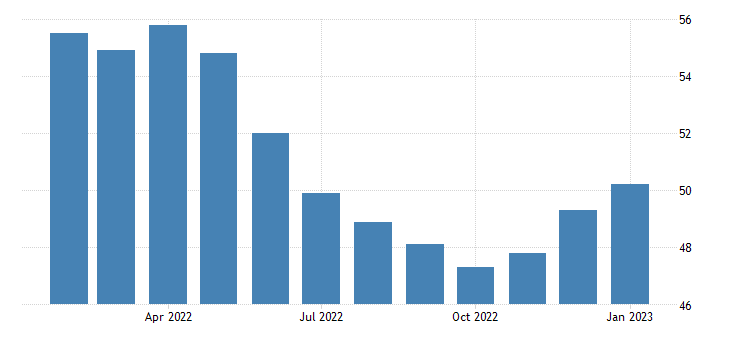

Eurozone PMI Composite Index rose for a third consecutive month in January, up from 49.3 in December to 50.2 in January, breaking above the 50.0 no-change level to thereby indicate the first expansion of business activity – albeit only marginal – since last June, according to a flash estimate from S&P Global.

The preliminary flash reading is based on approximately 85% of usual survey responses, covering both manufacturing and services.

January saw service sector activity rise for the first time since last July (the services business activity index rose from 49.8 to 50.7) while manufacturing output contracted only modestly (the index up from 47.8 to 49.0), registering the smallest drop in factory production since last June.

Growth was driven by technology (both IT services and equipment), as well as healthcare and pharmaceutical sectors, though industrial services also rebounded into growth territory.

However, downturns also eased in financial services, notably including real estate, and in basic resources sectors, while consumer-facing sectors such as tourism and recreation and household goods showed signs of stabilising after several months of decline.

Within the euro area, Germany reported only a marginal drop in output, the composite PMI rising from 49.0 in December to 49.7, its highest since output began falling last July, led by a marginal return to growth of services activity.

While manufacturing output continued to fall at a rate unchanged on December, the decline remained far less marked than recorded last autumn.

Output meanwhile fell for a third successive month in France, the composite index slipping from 49.1 to 49.0 to indicate a marginal steepening in the rate of decline. A cooling in the rate of manufacturing decline was countered by a sharper fall in services activity.

Euro Area Composite PMI. Source Trading economics

Output meanwhile returned to growth across the rest of the eurozone as a whole after four months of decline, led by the steepest rise in service sector activity for seven months and a near-stabilisation of manufacturing output.

The marginal return to growth of output across the eurozone as a whole was accompanied by a sharp improvement in optimism about the year ahead.

January saw the largest monthly increase in the eurozone PMI composite business expectations index since June 2020, building on gains seen in the prior three months to push confidence to its highest since last May.

Sentiment improved in both manufacturing and services, rising across France, Germany and the rest of the eurozone as a whole.

Some encouraging news regarding near-term prospects was also provided by the survey data on order books. Although new orders fell for a seventh straight month, the decline was the smallest recorded over this period.

New business placed at service providers fell only marginally while new orders for manufactured goods decreased at the slowest rate since last May, albeit still declining sharply.

Similarly, although backlogs of orders continued to fall – dropping for a seventh straight month – the decline was the shallowest since last October.

Companies met this brightening of business prospects and moderating decline in demand with additional hiring.

Employment rose at the fastest rate for three months in January, accelerating in both manufacturing and services, albeit with the rate of job creation remaining much weaker than seen this time last year.

By country, jobs growth picked up across the board, led by Germany. Factories meanwhile reported unchanged supplier delivery times for a second successive month, contrasting with the deteriorating supply picture seen over the prior three years.

Delivery times notably improved for a third straight month in Germany (though worsened in France). Supply chain stress has eased in part due to falling demand for inputs, which declined steeply again in January (though to a lesser degree than in each of the prior three months), which in turn is linked to a developing shift away from inventory building to inventory reduction.

Both stocks of factory inputs and finished goods fell in January, dropping for the first times in 16 and eight months respectively.

The easing of supply chain pressure helped alleviate input cost inflation, as did the calming of energy markets, especially in manufacturing.

Measured overall, input prices rose in January at the slowest rate since April 2021 – albeit still running well above the survey’s pre-pandemic long-run average.

However, manufacturing input cost inflation has now fallen below its pre-pandemic average, down to its lowest since October 2020, and service sector input cost inflation has slipped to a 13-month low.

Although input cost inflation slowed, average prices charged for goods and services rose at a slightly steeper rate than in December, with rates of inflation edging higher in both manufacturing and services.

While in both sectors the rates of increase remained off recent peaks, the sustained upward pressure on selling prices in part reflected efforts to rebuild margins, notably in the face of historically high energy and other raw material costs, as well as growing staff costs.