Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

Eurozone inflation is stickier than expected and is moving into double digits for the first time ever, as the ongoing energy crisis continues to push prices up across the board.

Monthly increases were also worse than expected and while energy prices have a large impact here, food and core inflation also went up.

While an increase was expected due to Germany reversing the nine euro public transport ticket measure from this summer, this jump was more broad-based than expected and will provide extra fuel for ECB hawks as we head into the October meeting.

While the ECB sees more demand-driven inflation at the moment, weaker consumer spending makes this limited at best. Perhaps in sectors still profiting from post-pandemic catchup demand this could be the case, but tourism-driven services in France actually saw weaker inflation than expected in September.

Most of the higher core inflation reading is still coming from second-round effects from the energy crisis, which is supported by the fact that businesses more dependent on energy have indicated they will increase prices in the months ahead.

The differences in inflation between countries are becoming more significant as measures at the national level are starting to complicate the overall picture.

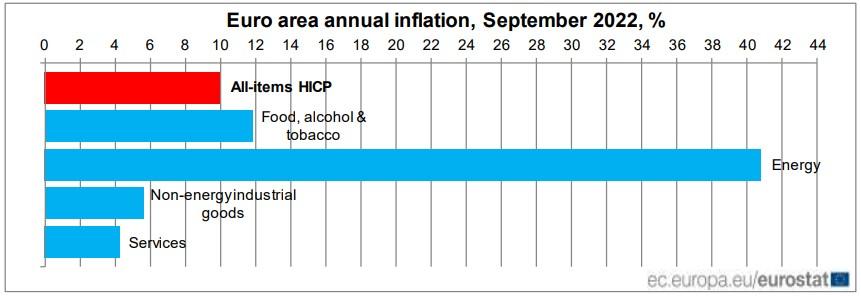

Looking at the main components of euro area inflation, energy is expected to have the highest annual rate in September (40.8%, compared with 38.6% in August), followed by food, alcohol & tobacco (11.8%, compared with 10.6% in August), non-energy industrial goods (5.6%, compared with 5.1% in August) and services (4.3%, compared with 3.8% in August).

As mentioned, Germany’s public transport measure pushed inflation up in September, but France saw a declining inflation rate mainly due to government measures aimed at improving purchasing power.

Expect government intervention to intensify on the back of still soaring inflation rates, and as long as this is not coordinated in Brussels, expect a continued muddied overall picture in the eurozone.

The divergence between countries would normally complicate the picture for the ECB, but with current high inflation rates the trajectory is clear: the ECB is set to hike drastically at the coming meetings to get to neutral and possibly beyond quickly.

First stop is the October meeting where another 75 basis point hike is now the most likely outcome.

Based on an analysis by ING Bank N.V. as copyright owner