Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

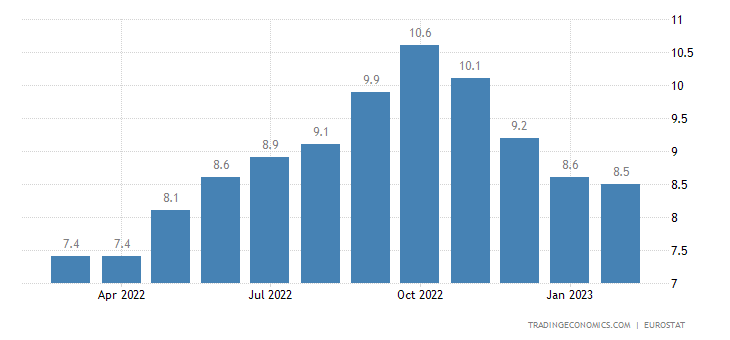

Inflation in Euro Area decreased slightly from 8.6 to 8.5% in February, but core inflation raised to 5.6%. While some forward-looking indicators for inflation are improving, the faster pace of underlying inflation means the European Central Bank has no reason to stop hiking anytime soon.

According to an analysis from ING Bank, the small decline in headline inflation mixed with a jump in core inflation is far from what the ECB had been hoping for.

The increase in food inflation stands out, jumping from 14.1 to 15% in February. Services inflation is also a clear worry, which increased from 4.4 to 4.8%.

With wage growth on the rise, concerns are that services inflation could prove sticky at high levels. But also energy inflation did not drop in line with the market price developments, thanks in part to French changes in the tariff shield.

The silver lining is that core inflation increases were mainly due to base effects.

″Using our own seasonal adjustment, we find that the monthly increase in core prices was in fact slightly down from January. So perhaps not as alarming as it looks at first sight, but then again, at 0.5% month-on-month, core inflation is still growing at an annualised pace above 6%. So still nowhere near the ECB target for the moment,” said Bert Colijn Senior Economist, Eurozone.

How bad is this exactly?

The February reading is a clear setback, but forward-looking indicators show that the declining trend in inflation is set to continue.

March will show a much faster drop in headline inflation as the huge jump from last March will fall out of the year-on-year comparison.

Energy inflation is set to turn negative soon, possibly already in March. But the question is how fast other price categories will see declines and if inflation proves to be stickier than expected.

We do see producer prices for food showing smaller increases and outright declines in food commodity prices, which should lead to slower consumer food inflation over the course of the year.

Goods inflation is also set to fade in the months ahead as input costs have improved markedly and selling price expectations from manufacturers are falling quickly.

The big worry to us is around services inflation as faster wage growth could make services inflation sticky.

Still, the smaller-than-expected decline in inflation in February is important as the ECB takes current underlying inflation seriously as a factor for determining policy.

That was not lost on markets this week as yields surged on the back of the higher inflation readings from Spain, France and Germany already released earlier.

At the same time, it is also important not to put too much emphasis on this one figure. A rate hike at the March ECB meeting is more or less a given at 50 basis points and May is still quite some time away.

There is a clear risk of the ECB having to do more, but ECB Chief Economist Philip Lane also indicated earlier this week that a lot is pointing in the right direction for inflation to come under control.

The difference between disappointing current inflation and optimism about forward-looking indicators will likely bring about more debate between hawks and doves ahead of the post-March meetings.

Before May, we will have quite some data to judge as to whether February was a blip or inflation does indeed remain stickier than expected.

With the courtesy of ING Bank as copyright owner