Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

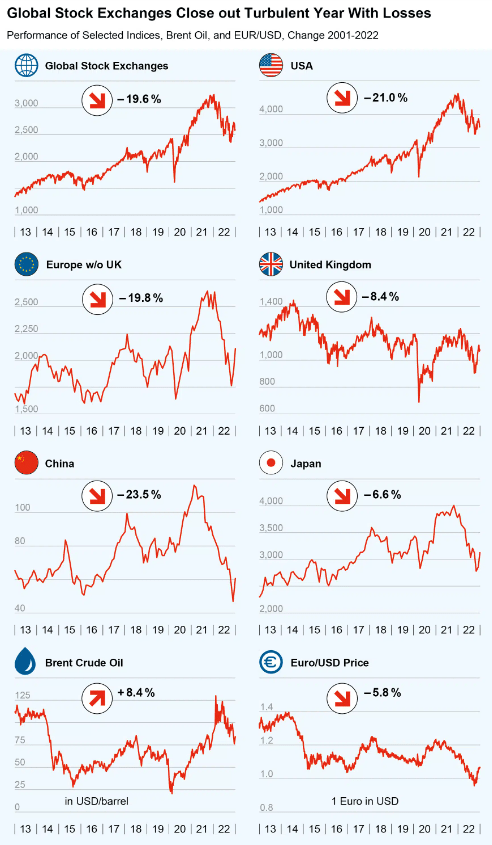

Last year turned out to be difficult and lossy for the stock markets. After a pandemic 2020-2021 and Russia’s invasion of Ukraine 2022, many stock exchanges suffered double-digit losses.

MSCI World Index, the benchmark for global stock market performance, slipped by almost 20 per cent over the course of the year, the US Dow Jones stock index and the Japanese Nikkei each down by around 9 per cent while Euro Stoxx 50 lost nearly 11% in 2022.

Oil and energy price increased because of the war, together with the economic recovery during spring, caused inflation to soar. At the beginning of 2022, the price for a barrel of Brent crude (159 l) was still just under 78 US dollars.

Immediately following the invasion, the price for Brent shot up to over 100 dollars, nearing the 120-dollar mark at times.

Of course, the beneficiaries of the oil price increases were oil company shares. Shares of US energy company Chevron were the Dow Jones’s top gainers, with 53% annual gain in 2022.

Shares of oil giants BP and Shell climbed to the top of the FTSE with gains of nearly 40 per cent at London Stock Exchange.

At the same time, the Ukraine war and the resulting fears of energy shortages in many countries accelerated the trend towards sustainable and renewable energies, but also the reconsideration of nuclear power.

Source: Erste Asset Management Blog

The price increases also fuelled fears that the central banks would react to the high inflation by raising key interest rates after a long phase of record-low interest, ending the era of cheap money for the immediate future.

Federal Reserve already raised its interest rates seven times in the past year and recently signalled further interest rate increases. The Fed’s key interest rate now lies between 4.25 and 4.50 per cent while European Central Bank proceeded somewhat more cautiously with four rate hikes.

All other central banks are currently presented with a difficult balancing act: on the one hand, they are trying to keep price increases in check by raising interest rates, which is also intended to prevent negative effects on consumer sentiment and thus on the economy.

But increasing interest by too much would have a negative impact on the already shaken economy.

A fair number of technology shares came under strong pressure with the interest rate turnaround in the past year. Tech companies need money for expensive investments that only pay off in the future and therefore suffer particularly from interest rate increases.

In the US, the tech-oriented Nasdaq Composite Index lost around 33 per cent over the course of the year, performing significantly more poorly than the Dow Jones.

Monetary policy remains a major theme for the new year. However, the latest figures show some hope. The eurozone’s inflation rate decreased slightly to 10.1 per cent in November after having reached a record high of 10.6 per cent in October.

Inflation is also expected to have peaked in the USA. Many economists expect the central banks to end their series of interest rate hikes in 2023.

This is also supported by the recent energy price developments. Oil prices recently pulled back significantly, with price for Brent hovering around 82 USD at the turn of the year.

At the end of the year, the European gas price continued its recent decline thanks to unusually mild winter temperatures. On Monday, the TTF futures contract for Dutch natural gas started trading at 70.30 EUR per MWh, marking the lowest natural gas price since before the start of the Ukraine war.

The latest economic data also gives hope for a good year. In Q3 of 2022, the US economy grew faster than previously forecasted. Gross domestic product (GDP) increased by 3.2 per cent for the year. However, good economic data is currently being received with mixed feelings on the markets, as it also may lead to further interest rate hikes.

In the eurozone, GDP grew by 0.3 per cent in Q3 compared to the previous quarter, and while many experts expect a temporary recession in the winter, recent surveys suggest it could be weaker than originally assumed.

The S&P-Global Purchasing Managers’ Index for the private sector recently increased by a full point to 48.8 points and is now approaching the 50-point mark that divides recession from economic growth.

Therefore, some economists do not want to rule out a positive surprise in the new year.

Article based on a story from Erste Asset Management