Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

The Federal Reserve voted today to raise the Fed Funds target rate range by 50bp to 4.25-4.5%, in line with market expectations.

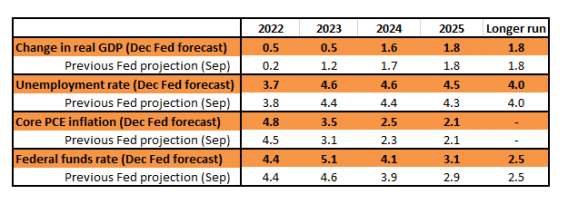

But more important is the fact that officials anticipate “ongoing increases” in the Fed Funds rate to be “appropriate”, while its forecast update has the central projection being for the Fed funds rate to end 2023 at 5.1% and 4.1% for 2024. They were 4.6% and 3.9% previously.

Two consecutive undershoots of inflation have led the market to believe we are getting very close to the peak for interest rates, and rate cuts will soon be on the agenda. But the Fed clearly isn’t willing to make that call.

There are some big upward revisions to the central bank’s inflation forecasts. Remember the Fed focuses on the core personal consumer expenditure deflator and not the core CPI which was published yesterday.

Core CPI is more impacted by used cars and has a different definition of medical care costs, both of with contributed significantly to the downside CPI miss. The core PCE deflator is likely to be stickier than core CPI with the Fed revising up its core PCE estimate to 3.5% for the end of 2023 versus 3.1% previously, with 2024 revised up to 2.5% from 2.3%.

The Fed is seemingly predicting only a modest downturn in activity next year with the unemployment rate rising to 4.6% from the current level of 3.7% with the economy continuing to expand, albeit at just 0.5% year-on-year between the fourth quarter of 2022 and the fourth quarter of 2023.

Source: Federal Reserve, ING

Another 50bp hike in February – the Fed wants more evidence that inflation is slowing

This relative hawkishness likely stems from concern that the recent steep falls in Treasury yields and the dollar are undermining the Fed’s interest rate hikes by loosening financial conditions – the exact opposite of what the Fed wants to see as it battles to get inflation lower.

Indeed, comments from Fed Chair Jerome Powell emphasise that the bank wants financial conditions to “reflect the policy restraint that we’re putting in place”.

After all, inflation is indeed still running well above target, the jobs market and wage pressure remain hot, and activity data is pointing to a decent fourth-quarter GDP report after a healthy 2.9% growth rate in the third quarter.

While the market may view inflation as being in its death throws, the Fed certainly does not. For the Fed to relax it will want to see substantial evidence that inflation is slowing, not just one or two months where core inflation has come in less than the market was expecting.

We must remember that to get inflation to 2% YoY over time we need to see month-on-month readings averaging 0.17%. We are not there yet and remember it is the core PCE deflator that the Fed pays the most attention to.

Given this situation, we should see another 50bp rate hike at the 1 February Federal Open Market Committee meeting.

With the courtesy of ING Bank as copyright owner