Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

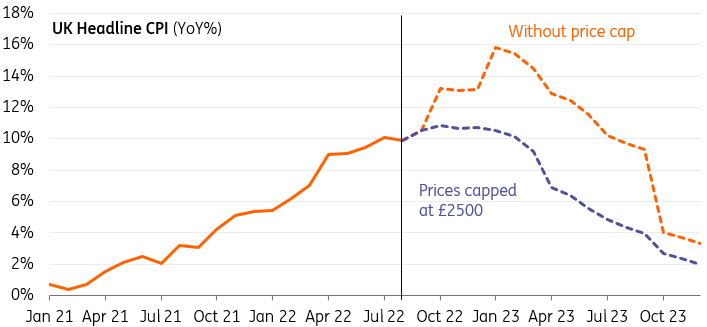

Headline inflation (i.e. a measure of the total inflation within an economy) is set to rise a little further having eased back below 10% in August, and it’s likely to stay around 11% in the first quarter of 2023, before falling back more dramatically.

However, the Bank of England is watching wage growth more closely, as the hawks worry that worker shortages could lead to core inflation staying more persistently above target, according to an analysis made by ING Bank.

„The absence of another upside surprise to UK inflation this month takes a bit of pressure off the Bank of England to move even more aggressively when it meets next week. Headline CPI came in a touch lower than both consensus and last month’s level, at 9.9%, and that’s largely because of a near-7% fall in petrol/diesel prices during August. We expect another 2% decline in next month’s figures,″ said James Smith, Developed Markets Specialist within ING.

The introduction of a government cap on household energy prices means that it would now be fairly close to the peak in these headline figures.

The fact that electricity/gas bills won’t be rising by around 80% in October and a further 30-40% in January means that the peak in CPI should be around 5 percentage points lower.

With the government due to cap the average household energy bill at £2500, up from around £2000 now, a peak in inflation will probably show 11% in October.

We’d expect inflation to stay around there until early next year, before cooling more quickly as energy base effects kick-in. We think it could be more-or-less back to the Bank of England’s 2% target by the end of next year, crazy as that currently seems.

But what policymakers are more interested in is core inflation – or to put it more accurately, the more persistent parts of the inflation basket.

Here the news is mixed. On a month-on-month price basis, the increases in August do seem fairly broad-based. However, there are signs that ‘core goods’ inflation is easing off, linked perhaps to the rise in retailer inventory levels relative to sales. That’s a function of supply chains beginning to improve, and in some cases commodity prices having fallen, which is coinciding with reduced demand for goods.