Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

Nvidia Corporation (NVDA.US) is major semiconductor producer and also designs a wide range of products, including graphics cards also known as GPUs, central processing units (CPUs), data processing units (DPUs) and network interface controllers (NICs).

Nvidia is primarily known for its GPUs, which are the company’s core business. Wide selection of products enables Nvidia to operate on several markets such as gaming, data centers, professional visualization, autonomous vehicles and OEMs. Nvidia is a well-established player in the semiconductor industry.

The company’s solid finances combined with a strong position in key markets such as Data Center and Gaming provide significant long-term growth potential. But let’s focus on finances first

Nvidia’s Q4 financial results – gaming in retreat

Despite surpassing analyst expectations and the current enthusiasm surrounding AI, fourth-quarter financial results created even more uncertainty.

Gaming platform sales collapsed and accounted for about half of the revenue reported in the same period last year. At the same time, revenues from Data Centers remain at a high level, but the cloud computing segment is facing a slowdown, which may negatively impact future revenue growth.

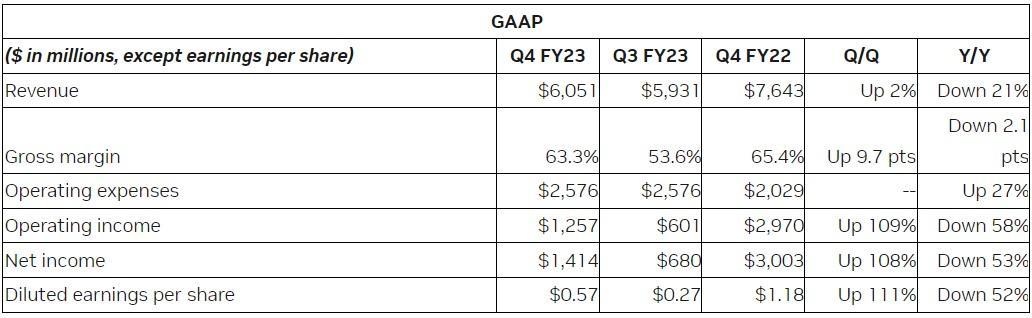

In the fourth fiscal quarter of 2023, the company’s revenue fell by 21% to $6.1 billion. The decline was driven by the gaming segment, which fell 46% YoY to $1.8 billion compared to $3.4 billion in the previous year as demand for games, especially in China weakens.

However, compared to the previous quarter, gaming revenue recorded an increase of 16% thanks to the company’s new graphics cards (GeForce RTX).

In addition, revenues from Professional Visualization and OEM & Others segments also plangad 65% and 56%, respectively. Lower sales were partially offset by higher revenue from the Data Center and Automotive platforms, which rose 11% and 135%, respectively.

Operating costs jumped 23% YoY increase which additionally weighed on the financial results. Research and development expenditures increased to $2 billion and accounted for 32% of revenues.

This lowered operating revenue by 40% to $1.8 billion compared to $3 billion in the same period last year. As a result, NVDA generated a net profit of $1.4 billion with a profit margin that was almost halved to 23.4%.

The king is dead (gaming), long live the king (Data Center)?

While revenues from the gaming segment are declining, the Data Center platform provides support for Nvidia. The revenue from this segment increased by 11% compared to the same period last year, which was driven by US cloud service providers.

However sales in China weakened, which was also reflected by lower cloud revenues from the country’s leading cloud computing providers.

Automotive revenue saw impressive triple-digit revenue growth, led by self-driving and computing solutions designed for EV manufacturers. This trend is expected to accelerate in the future, which may boost revenues in the coming quarters.

Temporary slowdown of the gaming sector

The slowdown in the gaming industry persists. In terms of generated revenues, the gaming segment has slowed down significantly over the past quarters and, according to the recent quarterly report, accounts for 30% of total revenues.

This is a significant difference compared to previous year, when this sector accounted for almost half of the company’s revenues. The announced partnership with Microsoft and Activision Blizzard could boost revenue, but the gaming market as a whole will need to see a stronger rebound before sales from the gaming sector return to previous levels.

Data Center revenue growth may slow down

Data Center continues to be a tangible and significant source of revenue for Nvidia. However, it is no secret that the cloud computing market slowed down in the last quarter, and the main providers of these services recorded a decline in growth dynamics. In addition, Chinese cloud computing service providers recorded flat or insignificant revenue growth.

Conclusions

Despite upbeat quarterly results and the current enthusiasm around AI, the company’s future performance is rather uncertain. Revenue decreased in three of its five segments, inventory levels have doubled within 12 months, and the cloud computing market could experience slowdown in the coming months.

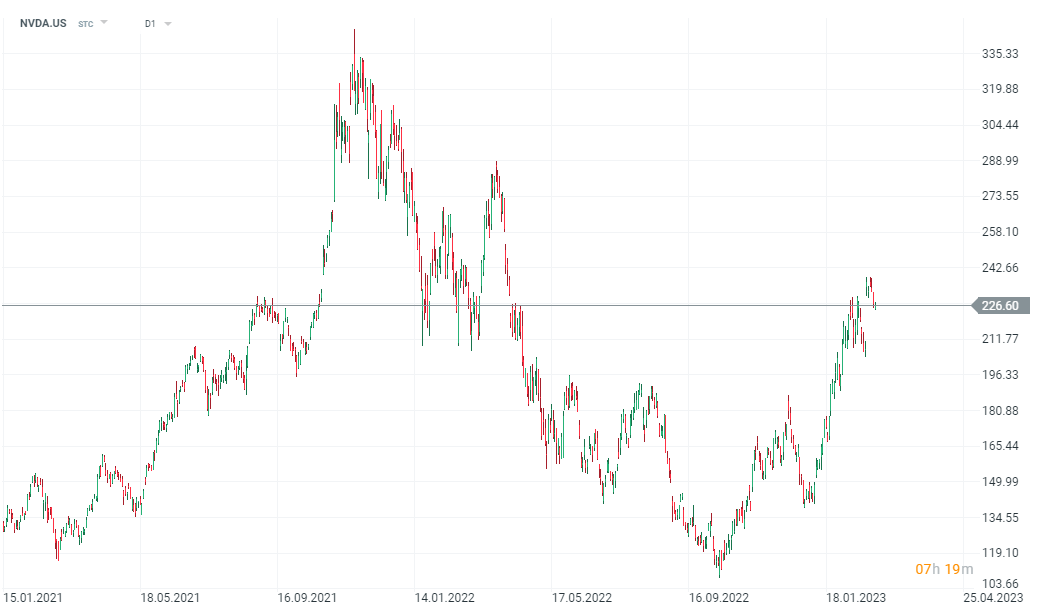

In addition, concerns regarding upcoming economic slowdown are on the rise. Nvidia stock price rose sharply in recent months, however given uncertain macroeconomic outlook many investors may decide to book profits, which in turn may spark a deeper downward correction. Nevertheless in the long term, it seems that the company has not yet said the last word.