Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

The return of Bob Iger, the chairman who brought shareholders a return of more than 550% in his 15 previous years in charge of Disney, has been positively received on Wall Street.

The CEO is a kind of symbol of ‘prosperity’ and is responsible for a powerful part of the company’s current shape. This, however, has been somewhat altered since Bob Chapek, who was removed from his post in November, took over.

When money is ‘cheap’ it is easy to spend. This is more or less how Chapek’s short tenure can be described.

Ultimately, the massive scale of spending has put a strain on share valuations in the face of a cash-intensive and loss-generating stream and uncertainty about the global health of consumers, hit by inflation.

Although cautious in his forecasts, Iger, in a conversation after the Q4 2022 results, did not prepare shareholders for any cataclysmic event.

On the contrary, the CEO hinted at a possible payment of a small dividend for 2023, with the potential to increase it in subsequent years.

After all, the company had been growing for more than 100 years, why should it disappear due to the fact that too much money had been spent in it for a while?

Iger did not like the financial ‘idyll’ of the Disney Media and Entertainment Distribution division, which included ‘good friends’ of former chairman Bob Chapek.

Bob Iger has decided to make 7,000 employees redundant, with the disbanded division mainly affected. Iger wants to do away with unnecessary expense-generating structures and make these more controllable at the end of the day.

This will potentially help the company even if the economic climate deteriorates significantly. The positive reaction of the markets to the redundancy decisions – this is the change that is taking place on Wall Street before our eyes. Investors are starting to like austerity. Iger too, has created a plan to save $5.5 billion.

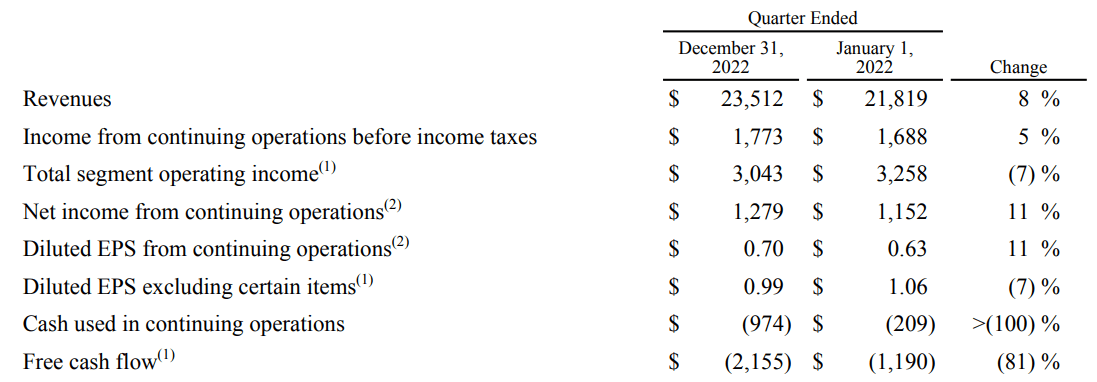

For Q4 2022, Disney delivered revenue of $23.51bn against $23.44bn forecasts and earnings per share that beat expectations by more than 10%.

However, nothing beat the result from the ‘good old’ theme parks, where it reported $8.1bn in revenue against profits of $3.1bn. Disney is associated with almost all existing generations for its original, immersive content.

So Iger announced a return to iconic brands and a base line of revenue – parks and big, proven productions. The CEO is clearly a man with a ‘flair for business’. – Soon, the theme parks will help monetize the huge success of Avatar: Creature of Water with new attractions.

This is how Disney wants to multiply profits from the content it has built. Avatar is not an isolated case. The most important thing? Not to overpay.

Iger will not be saving money on the already announced sequels to Toy Story or Frozen, on which the next new generation of little ones will be raised.

He also intends to focus on the strongest global franchises – Star Wars, Marvels and Pixar Animation Studios. But rest assured, Disney will be making savings wherever profit is uncertain.

Disney+ posted a massive nearly 1.5bn loss and a 2.4m outflow of subscribers, which now stand at 161.8m. At the same time, Netflix has seen them grow.

Analysts had expected the loss from streaming to be lower and the number of subscribers to be higher. The streaming business carries the risk of high competition, and the ‘whimsical choices’ of consumers being able to pick and choose from multiple platforms’ offerings.

While Iger obviously intends to drive Disney+ to profitability, he has outlined a significant restructuring and cost-cutting plan with which he has improved sentiment.

The CEO skilfully ‘played’ on investor emotions by creating a narrative, of streaming as an ‘add-on’ with long-term potential. After all, it wasn’t streaming that had made the company profitable for decades.

‘New ways’ of making money are not at all superior to old ways. Especially at a time when you have to seek profits from activities that require little investment. Finding the right way to do this is a major challenge for Disney today.

But a strong brand and demand in the theme parks should help and convince consumers to want to ‘overpay’ for the iconic company’s products. Often for the happiness of their own children, and that is, after all, almost ‘priceless’, right?

While the company could certainly be hit by a global recession, this one is still not a foregone conclusion – at least not in the US. Since the US economy is very strong and North American revenues account for the vast majority of Disney’s sales, even with a sizable slowdown in Asia or Europe – it is hard to expect a catastrophe.

Forecasts of the future are always subject to the risk of error because the future is unknown, and looking at the situation today – Disney may be facing another opportunity for revival, with an experienced CEO identifying with the company and a powerful consumer base.

While alarming macro data may be a warning sign, the right captain for such a circumstance in the form of Bob Iger is in post.