Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

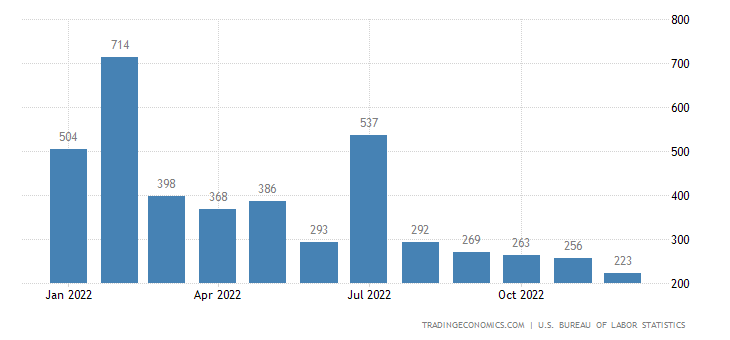

US economy added 223.000 jobs in December, above market consensus of 203.000 and shows that job growth was led by the service sector with education and health gaining 78.000, leisure/hospitality 67.000 and trade and transport gaining 27.000, while construction saw employment rise 28.000 with manufacturing up 8.000.

However, the economy is starting to see falls in some key areas, most notably temporary help, which posted the fifth consecutive monthly fall.

This is an important signal as these workers are always the first to be fired in a downturn (as they are the easiest to fire) and are likely to indicate broadening weakness in coming months. Business services fell for the second consecutive month while information services also saw employment fall.

Elsewhere, we have had quite a lot of revisions within the household survey, which is used to calculate the unemployment rate. It is now reported at 3.5% versus the 3.7% consensus.

This is down from a downwardly revised 3.6% in November (initially reported as 3.7%). While a great number, we need to remember that the low unemployment rate masks the fact that more that a third of the working age population are not engaged at all (participation rate is just 62.3%).

Then there are the wage numbers. Again there are major revisions, but this time they make the situation look a lot weaker. The annual rate of wage inflation (average hourly earnings) is now ‘just’ 4.6% whereas the market had been looking for 5%.

Last month’s 0.6% month-on-month initial print has been revised down to 0.4% while December’s MoM rate came in at 0.3% versus 0.4% expected.

Payrolls are broadly in line with expectations, the unemployment rate indicates strength, but wages indicate softening inflationary pressures.

Consequently, the focus switches to next Thursday’s CPI report. Markets are currently split between whether the Fed will raise rates by 25bp or 50bp at the February Federal Open Market Committee meeting.

Given the softer wage situation, if we get another core CPI print around 0.3% MoM or below, the case for a 25bp hike at the February FOMC versus 50bp is likely to build.