Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

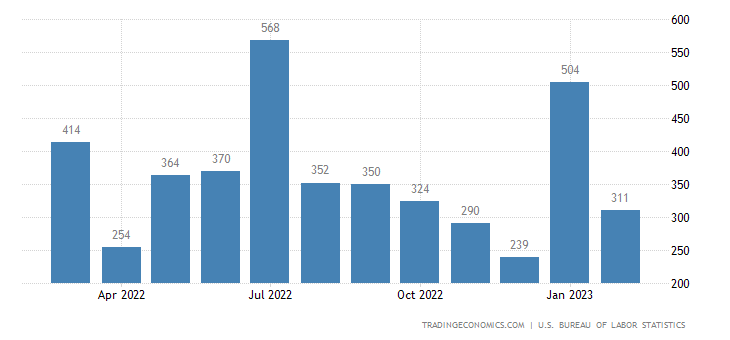

US non-farm payrolls rose 311k in February, above the 225k consensus, according to Bureau of Labor Statistics in USA. There were 34k of downward revisions to the past two months of data, but this is still a strong number.

A third of the jobs created were in the leisure and hospitality sector while retail added 50k, trade and transport rose 38k and private education/heath gained 74k.

Those sectors that didn’t do so well include manufacturing, which fell 4k and financial services, which was down 1k.

A big concern about the labour market is that, there is a big pick-up in lay-off announcements in well-paid, full-time sectors such as technology and financial services while the growth has been in lower paying, less secure, part-time sectors such as leisure and hospitality.

This caution remain valid, but at least this month we did see the job growth coming from full-time positions. Nonetheless, as the chart below shows, the number of full-time Americans in work has effectively flat lined since March last year.

Virtually all of the jobs created on balance over the past 11 months have been part-time, which isn’t a sign of strength. Therefore the composition of the jobs created is an important consideration in gauging the strength of the economy.

Full-time versus part-time employment levels (millions). Source: Macrobond, ING

Moreover, the report isn’t strong throughout with average hourly earnings coming in below expectations at 0.2% month-on-month/4.6% year-on-year and the unemployment rate ticking up to 3.6% from 3.4%.

Indeed the household survey showed employment rising a more modest 177k while the labour force grew 419k.

However, the labour market is a lagging indicator – it is the last data point to turn in a cycle – and the outlook is becoming increasingly challenging.

Certainly, we have been experiencing the most aggressive period of monetary policy tightening for 40 years and our long-term fears have been that the harder and faster you go into what we would term “restrictive” territory, the less control over the outcome.

As a result, we are constantly looking for signs of stress and clearly concerns about the stability of Silicon Valley Bank (SVB) and potentially other institutions are making investors nervous right now.

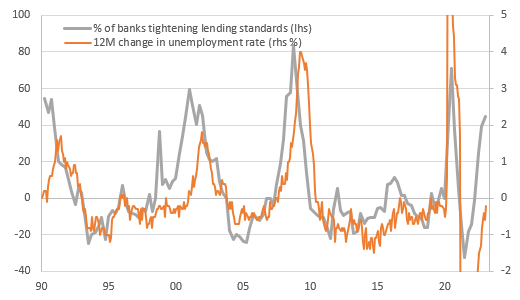

The January Federal Reserve Senior Loan Officer survey has shown banks are becoming much more cautious with the proportion tightening their lending standards having increased significantly over the past two quarters.

Therefore, we should not only be concerned about the rapid rise in borrowing costs, but also access to credit. Struggling companies and households are going to find themselves under intensifying pressures, with the chart below showing that typically when you see spikes in bank caution, the real world on activity and jobs isn’t far behind.

Senior Loan Officer survey shows banks are nervous and weaker credit flow means job losses. Source: Macrobond, ING

This then brings us to the question of what the Fed will do on 22 March. Chair Powell’s testimony clearly signaled that 50bp was firmly on the table and another strong jobs number will embolden the hawks on the committee.

Next week we have CPI, retail sales and industrial production. We think the two activity reports will be soft, but see little reason for the core CPI to come in below the 0.4% MoM consensus forecast this month.

This is still more than twice the rate needed (0.17% MoM) that would, over time, get us down to a 2% YoY inflation rate.

The macro newsflow and Powell’s testimony on their own would therefore suggest 50bp on 22 March, but market angst regarding Silicon Valley Bank and potentially others is unlikely to disappear.

If that’s the case a 25bp move would make more sense, especially given monetary policy operates with long lags and the cost and access to borrowing are going to increasingly weigh on the economy.

Article based upon analysis from ING Bank as copyright owner