Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

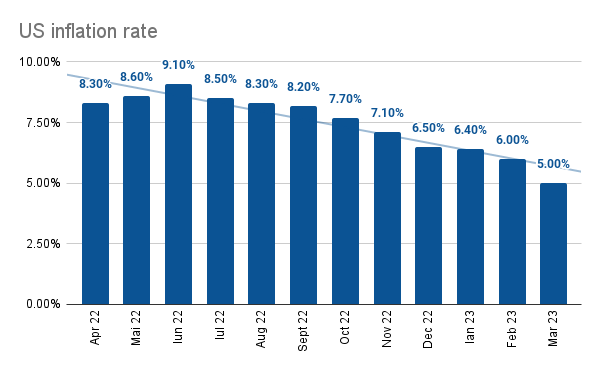

Inflation in the U.S. has slowed to 5% from 6% a year earlier, but monthly increases in non-food and energy prices continue to be stronger than desired, justifying the Fed’s decision to raise interest rates again in May.

U.S. consumer price inflation rose 0.1% in March from the previous month, below the expected rate of 0.2%, but core inflation CPI (excluding food and energy) remains high, rising 0.4% in the previous month, in line with expectations.

This means that the annual rate of core inflation increased from 5.5% to 5.6%, although the overall inflation rate decreased from 6% to 5%.

At 0.4% month-on-month (0.385% to three decimal places), the rate is still more than double the 0.17% month-on-month average required over an extended period to bring the annual core inflation rate back to the 2% target.

As a result, the odds remain good that the Fed will raise rates by another 25 basis points at the May 3 Federal Open Market Committee meeting.

Details show a 3.5% month-over-month decline in energy prices, led by a 4.6% drop in gasoline. Food prices were unchanged month-over-month, while transportation prices fell 0.5%.

With a 4% month-on-month increase, airfares continue to be a major factor in price increases, while most other components show signs of slowing.

Of particular note is the smaller contribution from the housing sector, where shelter prices rose 0.6% on average for the month and owner equivalent rents rose 0.5%.

This is slower than the imprints of 0.7% and 0.8% recorded last year, which is significant insofar as housing costs have the largest weighting within the basket of goods used to calculate inflation.

25 basis point hike in May, but cuts will come

Inflation remains above the 0.17% monthly average rate needed to bring year-over-year inflation to 2%, but we are moving in the right direction.

Still, the Federal Reserve remains nervous and seems inclined to raise rates again by 25 basis points at the May 3 FOMC meeting, marking the peak of the fed funds rate.

The combination of higher borrowing costs and tighter lending conditions that will inevitably result from the fallout of the recent banking crisis increases the risk of a hard economic landing.

This makes it even more likely that inflation will reach the 2% target again by early next year.

The Fed’s dual mandate of price stability and maximizing employment gives it more flexibility than most other central banks. Assuming that inflation moderates rapidly in the second half of the year and the unemployment rate begins to rise, the possibility of the Fed cutting rates by 100 basis points before the end of the year is resonable scenario.