Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

An average return of 13% a year to investors by the S&P 500 was the rule between 2013 and 2022, when ultra-low interest rates brought bigger gains in equities than in bonds.

In comparison, bonds issued by the same index listed corporations had annual returns of 2.5%, both in U.S. and Europe.

According to Reuters, the STOXX Europe 600 delivered annual returns of 8.1% against 0.8% for local investment grade bonds.

Europe is likely to keep the trend, where stocks will continue to be a better bet, while in the U.S. a fixed income resurgence this year could break through.

The central banks tightening to fight inflation have lifted government bonds’ yields to multi-year peaks, increasing the appeal of fixed income against equities.

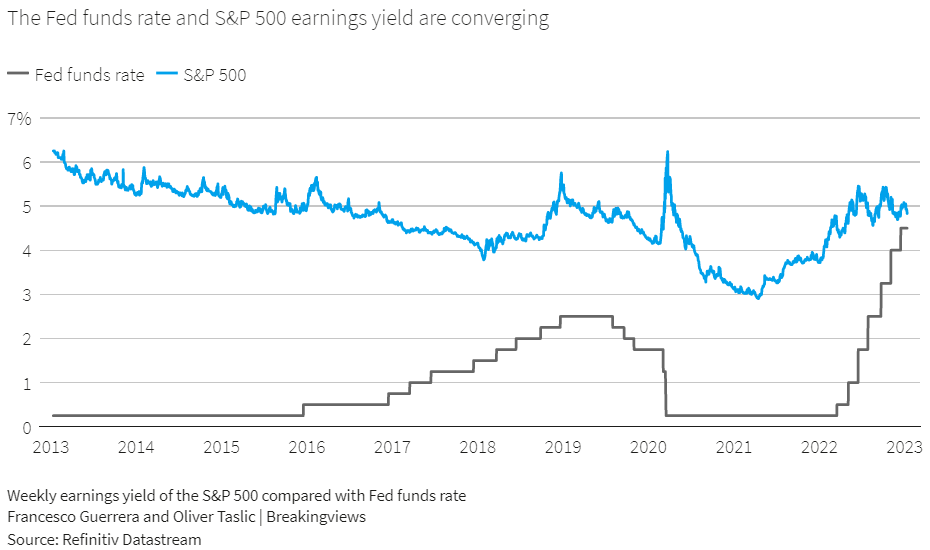

Now, the federal funds rate is between 4.25% and 4.5%, the highest in 15 years, while the S&P500’s earnings yield is at 4.83%.

With just about 30 basis points above the Fed funds rate, investors are not receiving proper compensation for the risk of investing in volatile stocks rather than cash or bonds.

On the other hand, the returns on the STOXX Europe 600 are more than 500 basis points above the 10-year German government debt yield, which stands at 2.2%.

Of course, the European Central Bank had a milder pace of increasing interest rates against the Fed, but European stocks are also cheaper than U.S. ones.

According to Barclays, in 2022, European shares had their biggest slide since 2018 and are trading 18% below their 10-year price-to-earnings median ratio.

In the United States, however, corporate valuations are now in line with their 10-year median ratio and 47% higher than European ones.

If a recession is milder than expected, European equities’ continued dominance could come to an end, especially if the ECB closes the yield gap between stocks and bonds through steeper hikes.