Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

Almost one year after the war started, the EU economy entered 2023 on a better footing than projected in autumn. The Winter interim Forecast lifts the growth outlook for this year to 0.8% in the EU and 0.9% in the euro area.

Both areas are now set to narrowly avoid the technical recession that was anticipated for the turn of the year. The forecast also slightly lowers the projections for inflation for both 2023 and 2024.

Following robust expansion in the first half of 2022, growth momentum abated in the third quarter, although slightly less than expected.

Despite exceptional adverse shocks, the EU economy avoided the fourth-quarter contraction projected in the Autumn Forecast. The annual growth rate for 2022 is now estimated at 3.5% in both the EU and the euro area.

Favourable developments since the Autumn Forecast have improved the growth outlook for this year. Continued diversification of supply sources and a sharp drop in consumption have left gas storage levels above the seasonal average of past years, and wholesale gas prices have fallen well below pre-war levels.

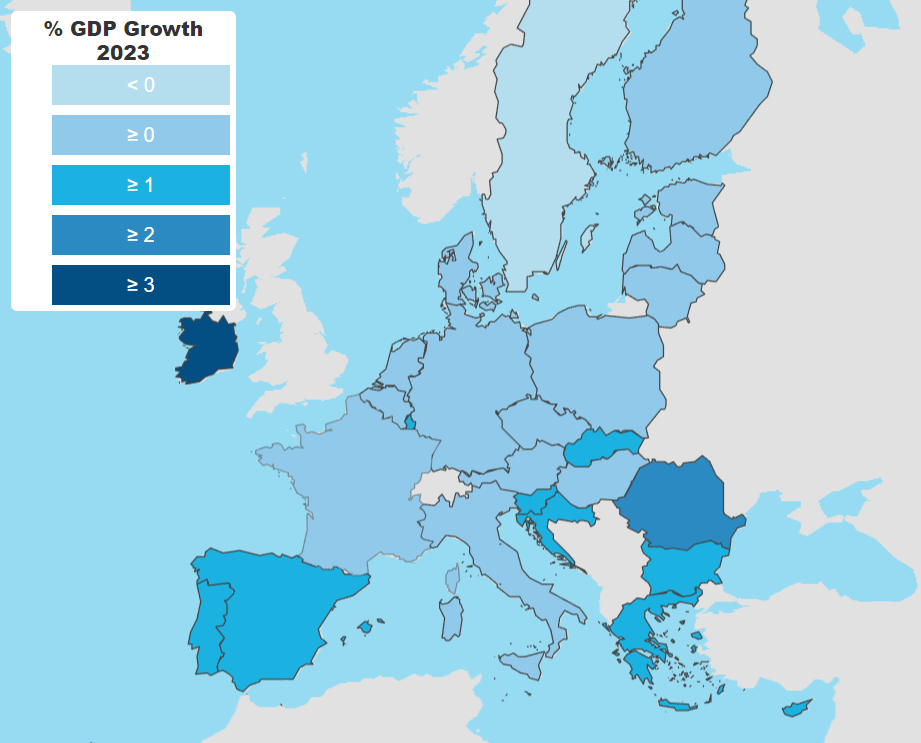

Euro GDP Growth 2023 (%)

In addition, the EU labour market has continued to perform strongly, with the unemployment rate remaining at its all-time low of 6.1% until the end of 2022. Confidence is improving and January surveys suggest that economic activity is also set to avoid a contraction in the first quarter of 2023.

Headwinds, however, remain strong. Consumers and businesses continue to face high energy costs and core inflation (headline inflation excluding energy and unprocessed food) was still rising in January, further eroding households’ purchasing power.

As inflationary pressures persist, monetary tightening is set to continue, weighing on business activity and exerting a drag on investment.

The Winter interim Forecast’s projected growth for 2023 of 0.8% in the EU and 0.9% in the euro area is respectively 0.5 and 0.6 pps higher than in the Autumn Forecast.

The growth rate for 2024 remains unchanged, at 1.6% and 1.5% for the EU and the euro area, respectively. By the end of the forecast horizon, the volume of output is set to be almost 1 per cent above that projected in the Autumn Forecast.

Three consecutive months of moderating headline inflation suggest that the peak is now behind us, as anticipated in the Autumn Forecast.

After reaching an all-time high of 10.6% in October, inflation has decreased, with the January flash estimate down to 8.5% in the euro area. The decline was driven mainly by falling energy inflation, while core inflation has not yet peaked.

The inflation forecast has been revised slightly downwards compared to autumn, mainly reflecting developments in the energy market.

Headline inflation is forecast to fall from 9.2% in 2022 to 6.4% in 2023 and to 2.8% in 2024 in the EU. In the euro area, it is projected to decelerate from 8.4% in 2022 to 5.6% in 2023 and to 2.5% in 2024.

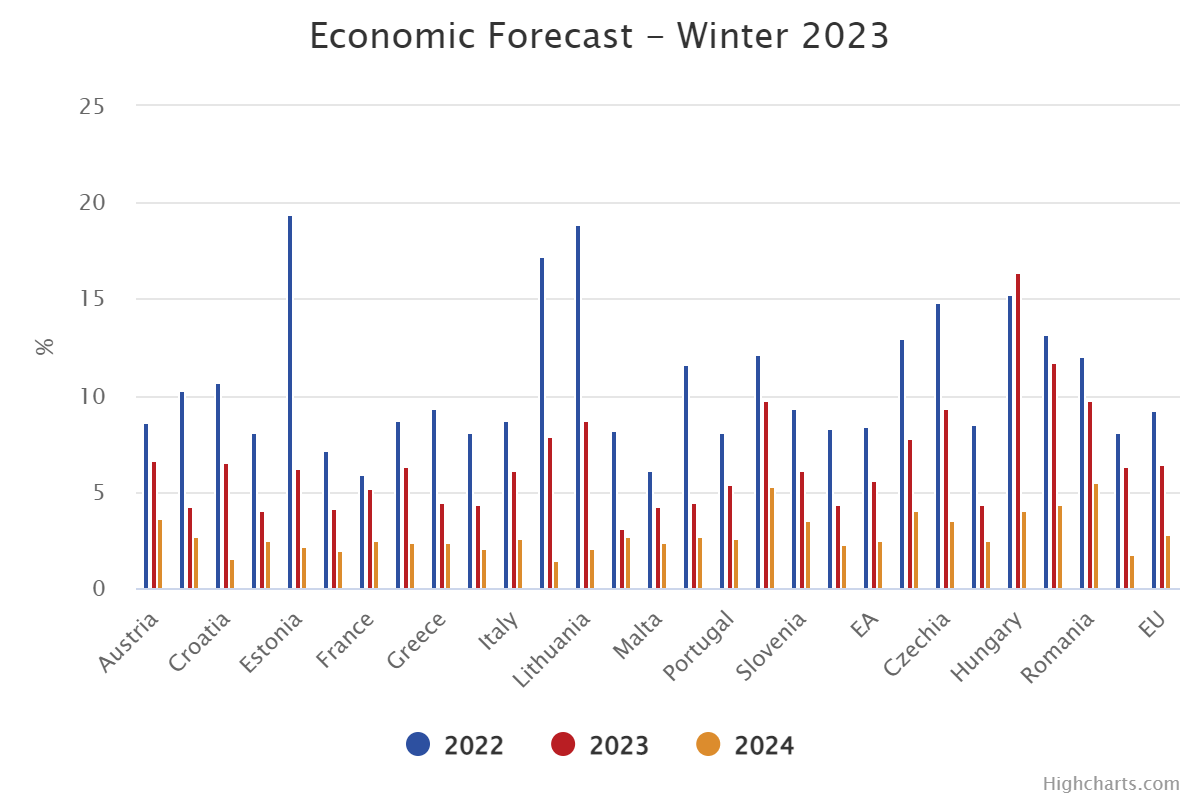

Inflation forecast

While uncertainty surrounding the forecast remains high, risks to growth are broadly balanced. Domestic demand could turn out higher than projected if the recent declines in wholesale gas prices pass through to consumer prices more strongly and consumption proves more resilient.

Nonetheless, a potential reversal of that fall cannot be ruled out in the context of continued geopolitical tensions. External demand could also turn out to be more robust following China’s re-opening – which could, however, fuel global inflation.

Risks to inflation remain largely linked to developments in energy markets, mirroring some of the identified risks to growth.

Especially in 2024, upside risks to inflation prevail, as price pressures may turn out broader and more entrenched than expected if wage growth were to settle at above-average rates for a sustained period.