Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

Recently, the scenario of a recovering global economy has become more likely. In line with the textbook, share prices have been up, and the prices of safe government bonds have been down. Moreover, the US dollar, inherently often anti-cyclical, has depreciated against a currency basket, writes Gerhard Winzer, Head Economist within Erste Asset Management, the fund administrator of Erste Bank,

But what are the main the reasons for this development and the necessary conditions for its continuation? Well, according to his opinion, first apperead on Erste Asset Management’s blog, the author identifies some positive reasons, argued below.

First of all, the outlook on an agreement in the conflict between the USA and China has improved. The agreement will probably not affect all areas of conflict (trade, technology, finance, currency, patents), and both countries might agree on a truce. This means that the downside risks (tail risks) for the global economy have decreased.[emaillocker]

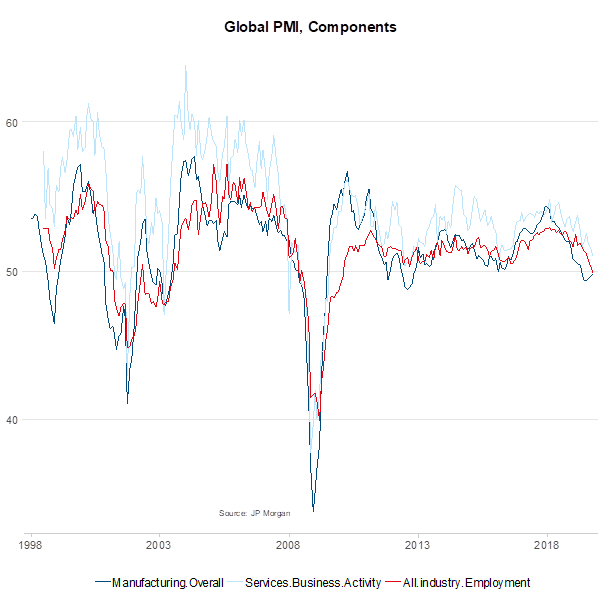

Also, the signs of stabilisation in the weak, i.e. hardly growing sectors of the global economy have increased. This applies to industrial production as well as corporate capital expenditure. The global purchasing managers’ index in the manufacturing sector is an important indicator in this context. In October, it recorded its third consecutive increase. The indicator that has recorded the most significant decline since the beginning of 2018, i.e. the sentiment in the business sector, has shown signs of bottoming out.

The central banks have re-embarked on (net) purchase programmes again and are buying government bonds. While the Federal Reserve only buys short-term T-bills, the effect of rising liquidity still feeds through to the market. The result is a looser financial environment (i.e. financial conditions), which means that many asset prices have increased over the year. This supports economic growth, albeit at a considerable time lag.

Also, fiscal policies have turned slightly looser as well. The relevant indicator in this case is the federal budget exclusive of interest payments, adjusted for the effects of the economic cycle in relation to the potential output of the economy. From 2018 to 2019, the aggregate figure for the OECD area declined by 0.4 percentage points to -1.4%. This has a marginally positive effect on economic growth.

As far as the credit environment is concerned, the development in China stands out. From the beginning of 2016 to the end of 2018, the credit impulse – i.e. the change in credit growth in relation to economic growth – was negative. On top of the increased geopolitical uncertainty and the reduction of global money supply, this was probably one of the main reasons for the weakening of global economic growth. Since the beginning of 2019, the credit impulse in China has been positive, albeit only slightly.

Source: Erste Asset Management

• The negative spillover effects from the weak to the currently strong sectors of consumption and services have to remain limited. On this front, the news flow is not particularly positive. Employment growth has already weakened, and the employment component of the purchasing managers’ index suggests a further decline. This means an erosion of the most important pillar of economic growth, i.e. private consumption. This means it is too soon for a trend reversal. Economic growth will probably remain low (i.e. below potential) for a few quarters.

• The assessment that the loosening of the monetary policy was sufficiently effective to stabilise the weakening of economic growth may be right. However, the central bank in the USA is signalling an end to its rate cuts (in total, 0.75 percentage points to a band of 1.5-1.75%), signalising other central banks to cut their key-lending rates. In other words: the global interest cut cycle is coming to its end. At the same time, Chairman Powell from the Federal Reserve has made it clear that the hurdle for rate hikes is equally high. The Fed might think about going down that road in the event of a sustainable increase in inflation, and less so in case of higher economic growth. Conclusion: the monetary policies have to remain loose.

• Company earnings have to grow again. In recent months, company earnings have fallen significantly worldwide. At the moment, they are stagnating. This has to do with revenue growth, which has declined just like nominal economic growth, and with the accelerating growth rate of unit wage costs.

• Due to the still tight labour market, many countries have seen their wage growth speed up. This is generally positive. However, since productivity growth is lower, unit wage costs have increased. Theoretically, this can translate into pressure towards higher consumer price inflation or on profit margins. The latter scenario has manifested itself in recent quarters. In a recovery scenario, the pressure on profit margins in the corporate sector falls, probably on the back of higher revenue growth.

Conclusion: the increase in risky asset prices is increasingly less due to rate cuts by central banks (as this cycle is coming to an end). Rather, it is based on the falling tail (downside) risks, driven by the outlook on a mini deal between the USA and China. For a trend reversal of economic growth, the negative spillover effects have to remain limited, and the central bank policies have to stay loose. At the same time, company earnings will have to pick up. This may take a few more quarters.

The article first appeared here.[/emaillocker]

[ajax_load_more]