Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

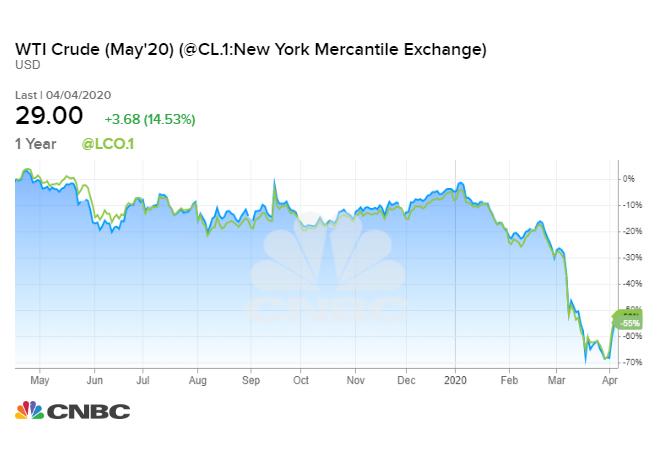

The most significant development on the markets this week was the increase of the oil price by around 40% to 34 US Dollars per barrel (Brent) and aroud 28 usd for WTI Crude. This development has (unfortunately) nothing to do with any recovery of the economy after the large drop over the last weeks.

The trigger for that development was a tweet by US president Donald Trump increasing the hope of production cuts. The OPEC+ oil alliance consisting of OPEC and Russia collapsed last month and has led to an abolishment of any production restrictions.

Therefore, the oil price dropped strongly and reached for some time the lowest value since 2002. That oil price shock is a small issue compared to the spreading of the coronavirus, however, for some companies in the shale oil sector in the USA that means existential problems and for some countries it can lead to a downgrading of their credit rating.

Shortly after the tweet of US president Trump Saudi Arabia has asked for an emergency meeting. But the creation of a new oligopoly, consisting of the USA, Russia and OPEC is not easily achievable. It would be a so called OPEC 3.0. That development should be kept in focus.

Even in the case of production cuts (in the Trump tweet 10 to 15 million barrels were mentioned) an increase of the oil price is not certain. The collapse of the oil demand due to the measures to restrict the spreading of the coronavirus is enormous. According to some estimates the reduction in demand is around a third of the total daily production volume of around 80 million barrels.

The economic indicators will confirm the drop in economic activity. The OECD sees a decrease of GDP as reaction to the containment measures of 20% to 25%. In the USA over the last two weeks around 10 million people have initially applied for unemployment benefits.

For the unemployment rate that reflects an increase to around 10%. In February it was only 3,5%. Positive is the decrease of uncertainty in regards to the extent of the economic crisis. Now it is all about developing a realistic scenario for the duration of the crisis as well as secondary effects. The latter describes among others how fast the unemployment rates decrease after the loosening of the containment measures.

WTI Crude (blue line) and Brent (green line) evolution

What will we be looking at over the next weeks?

As mentioned already several times currently there are two large forces on the capital markets. On the one hand the containment measures and its economic impact and on the other hand the fast and strong reactions by the governments (fiscal policy) and the central banks (monetary policy).

„We still assume the basic scenario that the markets will stabilize in a sustainable way as soon as the containment measures will be working, the economic consequences can be estimated and the fiscal- and monetary instruments start to work.”

In all three elements we got more certainty over the last few days. The incoming data look dramatic, markets react in the meantime only partly to them. The uncertainty decreases slowly and volatility will remain increased.

With the courtesy of Erste Asset Management as copyright owner. The article first appeared here.

[ajax_load_more]