Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

The months of November and December have traditionally always been the strongest months of the year on the stock exchange. The term “year-end rally” is sometimes used when prices are going up.

The year 2021 has been a positive one for equity investors so far. The S&P 500 index, the index tracking the 500 biggest listed US companies, has gained about 25% in the year to date.

Over the past five years, share prices have doubled on average (source: Refinitiv Datastream, as of 15 November 2021) despite the set-backs in the second half of 2019 and in spring of 2020 (the latter one due to corona).

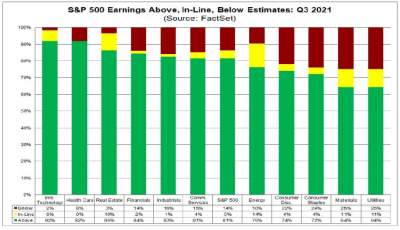

More than 80% of companies exceeded their earnings estimates

In this article, we want to discuss the fundamental factors that have been driving the strong performance. How did the companies really do?

Did they fulfil or even exceed their sales and earnings forecasts? In the USA, the Q3 reporting season is drawing to an end. By the beginning of the week, 92% of the S&P 500 companies had reported their results.

Despite the dampening factors such as rising inflation, the sharply increasing covid numbers, and the supply bottlenecks in the industrial sector (especially due to shortages in the semiconductor segment), US companies reported surprisingly good figures: 81% of companies exceeded earnings expectations, 75% also exceeded sales expectations.

Q3 2021 earnings growth increased relatively to its referential 2020 figure by 39.1% y/y (source: FactSet). The consensus had estimated an increase of 27.4%, which would have already been significant. Historically speaking, this was the third-best Q3 ever. All sectors recorded positive growth, belying all those who had foreseen a slump in the economy after the lockdown rebound.

Financials and energy sector on top

The financial sector recorded the biggest gap between expected and actual results, while the energy sector posted the biggest discrepancy between analyst consensus and sales growth. At 12.9%, profit margins fell slightly short of expectations, but they remained close to the record highs of previous quarters and well above the 5Y average of 10.9%.

Valuations above long-term average

The relatively high equity valuations are the only fly in the ointment. At currently 21.2x, the 12M PE ratio is substantially above both 5Y (18.4x) and 10Y average (16.5x). The price hikes – mainly, but not only, in the energy sector – have affected the analysts’ estimates: for the ongoing Q4 they expect profit growth to continue at about 20% and sales growth to remain above 12%.