Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

During the global pandemic, the most important central banks loosened their already expansive monetary policies further and thus stepped up money supply again.

They are doing everything to ensure that the global economy picks up momentum after months of hard constraints. This strategy has been particularly successful in the USA and in China.

Some sectors such as the semiconductor industry can hardly keep up with demand and, all of a sudden, inflation has become a topic. Investors who want to absorb a strong increase in prices can do so via various routes: with equities or with real assets such real estate or gold.

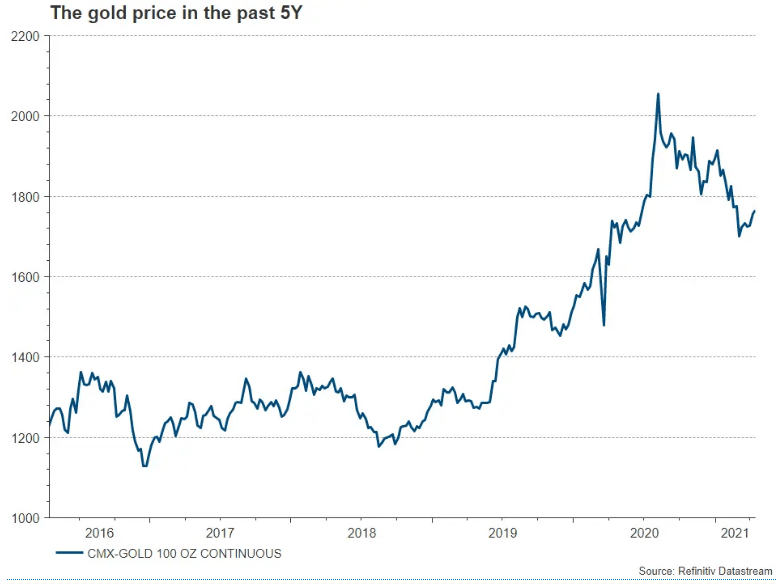

The gold price fell by 5.9% in the first quarter (in euro terms). Given that gold is an asset that is supposed to excel in stability, that is quite a bit. Has gold lost its shimmer?

We have to see the bigger picture here. In the almost five years from the end of 2015 to August of 2020, the price of gold nearly doubled.

The current consolidation in the wake of years of outperformance is therefore not all that surprising.

I would even call it healthy. Gold also outperformed most stock exchanges last year: the gold price (in USD) increased by 24%, whereas the broad US equity market only gained 16%.

What was the reason for the decline in Q1? What factors were decisive?

The decline of the gold price was largely caused by the fact that investors shifted their funds to a significant degree into riskier asset classes such as equities or corporate bonds in view of the expected economic development this year.

Gold was less in demand in such an environment. Government bond prices also came under pressure, which led to rising yields in the USA. This caused the opportunity cost of holding gold to rise.

Can you contextualise the topic of inflation – or inflation expectation – and gold?

The rate of inflation is higher and more volatile this year, which leads to fluctuating real yields. The lower real yields are, the more significantly the gold price reacts by spiking.

However, the price-driving effect is not as strong as it was during times of negative real yields. A drastic increase in yields is unlikely, given that the global central banks will probably not raise their key-lending rates for several more years due to the low rate of inflation. The massive volume of government bond purchases by the central banks will keep yields low.

How has gold demand developed in recent months?

We have a full set of data available until the end of 2020. In Q4 2020, demand was down 28% relative to Q4 2019. Due to the effects of the spreading of COVID-19 and the rise in the price of gold, jewellery demand fell by 13% during the same period of time.

However, the sales of bullions and coins increased by 10%. The global central banks stepped up their holdings marginally. Consolidation has continued this year: in March, global gold ETFs lost 107.5 tonnes (i.e. USD 5.9bn, or 2.9% of assets under management) and thus recorded an outflow in the fourth month of five.

According to the World Gold Council, assets held in gold worldwide amount to USD 194.5bn or 3,574 tonnes, which is equal to the numbers of June 2020. Since the high of assets held in gold in November 2020, holdings of ETFs have fallen by almost 9% in tonnes, which is more or less in line with the decline in the price of gold during that period.

Would you say that after its consolidation, the gold price has bottomed out? Could demand pick up in the coming months, and if so, why?

I have no crystal ball and there are driving factors that can change quickly, e.g. the surprisingly fast rise in US Treasury yields.

Gold is currently attractive mainly for reasons of diversification. An uptick in the volatility of equity markets in the coming months should result in the foreseeable stabilisation of the gold price.

We expect a slight increase in the price of gold for Q2 to a range of USD 1,750 to USD 1,780. In the long run, the gold price should move in a moderate upward. This means there is some upward potential.

With the courtesy of Erste Asset Management, as copyright owner. The article first appeared here.