Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

The world economy and global financial markets are in trouble. In addition to its disastrous medical consequences, the coronavirus pandemic is about to trigger a global recession with all its negative consequences like rising unemployment, overburdened social systems and rising bankruptcies.

And it has already lead to the most severe turmoil in the markets for risky assets since the Great Financial Crisis in 2007-08.

The roots of market collapses may vary, as we saw in the course of the last three big crashes in 2000 (bursting of the tech bubble), in 2007-08 (US mortgage crisis and the collapse of Lehmann Brothers) and the current virus-related crisis.

But regardless of the initial catalyst, the dynamics of markets on the way down as reflected in the performance of key equity indices, volatility indicators, prices of supposedly safe assets and currencies are often astonishingly similar.

The last crisis that is still fresh on everybody’s mind is the Great Financial Crises (GFC) that started in 2007 and accelerated in September 2008 following the collapse of Lehman Brothers. It led to a global recession, a destruction of 40-45% of global wealth according to some estimates and the introduction of hitherto not known monetary policy instruments and regulatory interventions.

The GFC, therefore, is probably the best reference point for any assessment of what is happening right now in financial markets and how things could play out in the months to come.

Corona vs. Lehman

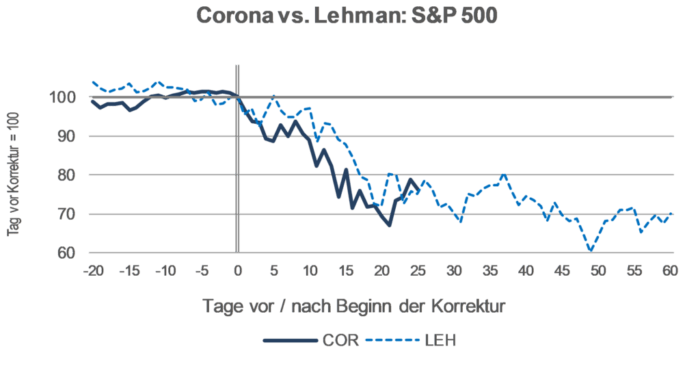

The 2008 crash had, similar to the current one, a massive impact across all asset-classes. One example is presented in the chart below, which shows the performance of the S&P 500 after Feb 21, 2020, when European and US financial markets started responding vehemently to the breakout of the coronavirus, in comparison to what happened after September 15, 2008 – the date when Lehman Brothers went bankrupt.

Source: Bloomberg; Erste Asset Management; data as of March 27, 2020.

Needless to say that such a comparison should not be confounded with a forecast. But the similarities might tell us what is possible in financial markets following a major shock like the coronavirus pandemic.

And the differences between the two crises may also provide clues on whether the current crisis could follow a different course as we go along.

Comparing the crises in 2008 and 2020 in more detail points to a number of noteworthy developments:

1. In the first five weeks, the coronavirus sell-off in global stock markets has been steeper and deeper than during the Lehmann-related crash, at least in Europe and the US. One notable difference is that in the twelve months prior to the collapse of Lehmann, global stocks had already lost more than 20%, whereas the correction last month came just few days after major equity indices had reached all-time highs.

2. In terms of relative performance Europe initially underperformed the US during the current crises. This has changed more recently though after the US has also been fully hit by the virus. Emerging markets have outperformed because the pandemic started receding in Asia but is still gaining momentum in developed markets. However, the experience in 2008 suggests that as soon as the global economic turbulences are severe enough, emerging markets cannot escape and may even be hit harder than the developed world.

3. Unsurprisingly, key volatility and risk indicators have reflected the stress related to the current pandemic. Equity volatility jumped to levels last seen in 2008. Likewise in bond and currency markets volatility has surged but has stayed well below levels during the 2008 crisis. But note that they came from very low levels at the outset of the crisis.

4. Other classes of risky assets have felt the heat as well. In the US, high-yield spreads – the gap between rates for non-investment grade corporate bonds and government bonds – have soared to over 1, 000 basis points – a level that in 2008 was reached only at a later stage in the crisis. The main reason for the swift rise this time was related to the shale oil industry, which is a prime victim of collapsing crude prices and, in the meantime, accounts for a significant share of non-investment grade bonds.

5. US bonds followed quite a different trajectory now and then. In 2020, the initial response was a drop in yields from already very low levels, while 12 years ago the market response to the deteriorating economic backdrop happened two months after the event. In both cases, yield curves steepened in the US as well as in Europe in anticipation of monetary easing by the central banks.

6. In both instances – 2008 and during the current rout – the US dollar strengthened after a few days of weakness, reflecting its status as a safe haven currency. However, during the current crisis this trend has reversed as of late as the coronavirus has taken hold of the US as well.

7. Gold has moved sideways in recent weeks, while in 2008 it gained almost 20% within few days after the Lehman debacle. It later posted a decline, which proved temporary though. Over the following three years gold rose by 140%, most likely in response to the unprecedented monetary easing by the US central bank, which triggered inflation fears (that were unfounded as we know now).

8. The price of oil has fallen about twice as fast this time around compared to 2008. In addition to the downward pressure due to the expected recession, the failure of Saudi Arabia and Russia to agree on production cuts has accelerated the price drop. In 2008, oil was already heading south before Lehmann, and Brent lost another 60% before it hit bottom at USD34/bbl three months later.

9. Consensus expectations both for economic growth and corporate profits have come down faster in the course of the coronavirus crisis than after Lehman. Given the experience back in 2008, and taking into account the fact that consensus forecasts are slow-moving indicators, one can expect further downgrades in coming weeks and months.

Uncertainty and volatility to remain elevated

Forward-looking valuation is right now an even less reliable indicator than in more normal times. Still, what the data show is that last week’s equity rally should not be mistaken for a sign that markets have already entered into calmer waters. Even if forward earnings multiples should have bottomed (a big if), further earnings revisions will continue putting pressure on equity markets.

One lesson from the GFC twelve years ago is that disruptions of such a massive order tend to have longer-term repercussions. Thus, also in the current crisis we may face bumpy ride ahead of us.

How should equity investors respond?

Another lesson from the last crisis, respectively from periods of elevated volatility in general is that market timing – i.e. the attempt to adjust your equity allocation based on daily and weekly markets fluctuations – has little chance of success.

Even in a volatile environment like now, regular investments in stocks are the best way to add to positions at low market prices and benefit from the possible recovery.

Author Peter Szopo, Chief Equity Strategist at Erste Asset Management, as copyright owner.

[ajax_load_more]