Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

A month of the Ukrainian government’s current financing needs amounts to €4 billion, while the effort needed when the time comes to rebuild the country exceeds €750 billion.

So Brussels embraces the idea of doing to Russia what the Kremlin did to Kyiv, and that’s ignoring bilateral treaties that protect individuals and, in this particular case, businesses against expropriation.

The European Commission’s plan is to use billions of dollars and euros of frozen Russian assets to help finance the reconstruction of Ukraine.

Also, the EU’s Executive wants for Kremlin to also pay somehow for the higher inflation and the major energy crises triggered by Moscow’s territorial ambitions.

Europe is also sending financial and military aid to Ukraine, so there’s a moral imperative to make the aggressor accountable.

Taxpayer fatigue is also taken into consideration since this could turn into revolt when the governments start footing the bill for Ukraine’s reconstruction.

Firstly, the EU is eyeing €19 billion worth of sanctioned oligarch’s money.

But besides breaking legal rules, some sanctioned oligarchs may already have transferred some assets to family-controlled trusts before the sanctions hit.

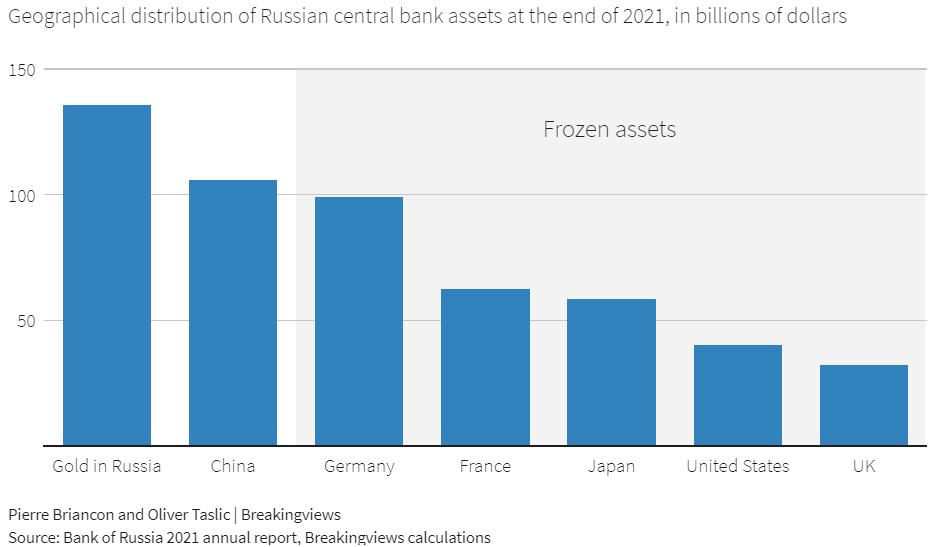

The EU is also targeting an estimated €165 billion of frozen Russian reserves sitting in eurozone central banks.

According to Reuters, there’s a moral dilemma in this plan since parties wronged by the Russian state could try to recoup their losses by making claims against the assets.

That’s the case of investors expropriated by the Kremlin over the years, or creditors if Russia defaulted.

Using only the financial returns from the assets to pay for Ukraine could be a smoother alternative, like investing in 10-year bonds.

But the gains would be marginal, far under Kyiv’s financing needs in a month.

Besides the shady aspect of breaching several treaties and property rights, this scheme also puts a burden on a future post-Putin Russia, fueling new frustrations with the West.