Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

European stocks have been rising for seven months, dwarfing their American counterparts. They are now just 6% below their record high, but companies in the region are running out of steam.

An unprecedented series of rate hikes will erode profits, margins and demand. The block still looks cheap, but for good reason.

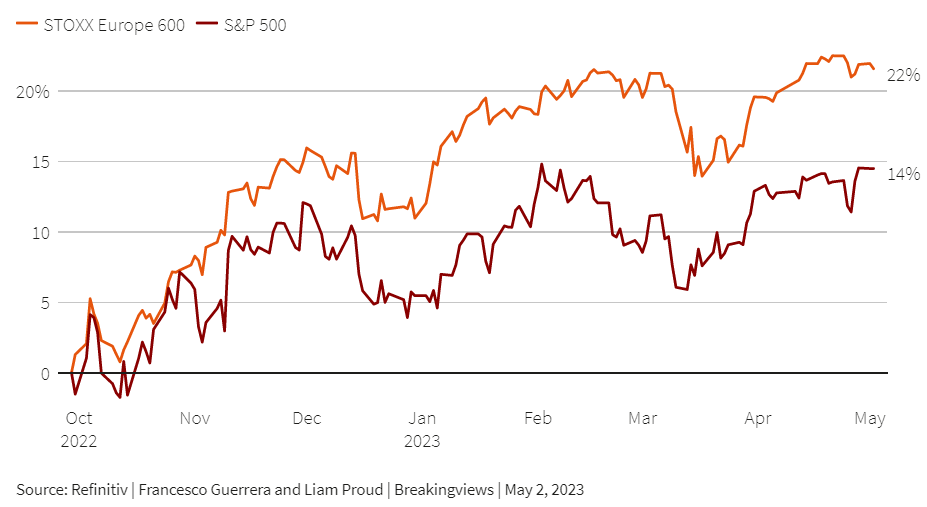

Investors in Europe have had an unusually good time lately. The STOXX Europe 600 Index is currently trading at around 460, close to its all-time high of 494.35 from January 2022, and has risen more than 22% since its recent low in late September, eclipsing the 14% gain in the S&P 500 Index of leading U.S. stocks.

This kind of outperformance is unusual – the last time it happened consistently was between 2005 and 2007. Since then, investors have focused on the larger, deeper, and more technology-heavy U.S. market.

Luck also played a role in Europe’s recent surge. The rise in energy costs caused by the Russian invasion of Ukraine has not led to the feared recession, in part because the winter was mild and governments sourced fuel from other countries.

Natural gas prices have fallen by more than 80% since their peak in August, boosting economic growth and reducing companies’ costs.

China has also helped. Beijing lifted draconian covid lockdown measures in December. Since then, the Middle Kingdom economy has been on the upswing. GDP grew at a 4.5% annual rate in the first quarter of 2023, boosted by domestic consumption.

This prompted investors to buy into European exporters. Shares of France’s LVMH, which generates 30% of its sales in Asian countries outside Japan, are up more than 25% this year.

The composition of European stock markets also played a major role. Nearly 40% of the region’s stock market is made up of so-called cyclical stocks such as banks and industrials, whose fortunes tend to rise and fall with the economy.

That compares to just 22% in the United States, according to JPMorgan. The current environment of high inflation, high interest rates and slow growth favours these companies because they can charge more for their products and services. Shares of UniCredit, a major Italian lender, have risen by more than a third since January despite the bank failures in the United States and Europe.

This favourable environment lured investors to Europe after years of indifference. What they found was a treasure trove of relative bargains.

Even after the recent surge, European stocks trade at 12.7 times next year’s expected earnings, a 30% discount to U.S. valuations, according to IBES estimates.

Now, however, the favourable winds will shift. First, economic clouds are gathering. To combat rampant inflation, the European Central Bank has raised interest rates from below zero to 3% in just eight months and they could reach 4% before the summer.

The drastic tightening of monetary policy will reduce growth to a trickle, dampening demand and curbing spending by households and businesses.

The ECB projects that the eurozone economy will grow only 1% in 2023, down from 3.6% last year. For 2024 and 2025, the central bank expects GDP to grow by a modest 1.6% in each year.

Higher interest rates and the tight situation in the banking sector will make it more difficult and expensive for companies to raise capital.

And the strength of the euro against the dollar will reduce the value of profits generated abroad and make European goods more expensive.

The single currency is trading around 10% higher against the dollar than on average last year.

These factors could cut into profits. According to Barclays, analysts currently expect European companies’ earnings per share (EPS) to decline by 0.4% in 2023, which seems too optimistic.

Graham Secker of Morgan Stanley estimates in a recent note that the strength of the euro alone could reduce earnings per share by 5%.

In addition, lower economic growth is likely to reduce demand and volume, while falling inflation is putting downward pressure on prices and reducing operating margins.

Under these conditions, earnings per share could fall by as much as 10% this year, Secker calculates. Once the bad news starts to emerge, shares could plummet.

Some investors are already shifting their trades elsewhere. Equity funds focused on Europe have suffered six straight weeks of outflows, according to Bank of America.

Actively managed funds focused on Europe saw outflows totaling more than $18 billion in 2023, but that was partially offset by inflows of $15.6 billion into passive funds that invest in the region.

Emerging market equities are a real alternative. They are cheaper than European stocks and trade at 12 times next year’s projected earnings, based on the MSCI Emerging Markets Index.

The recovery in China, high commodity prices and the weak dollar are likely to boost companies in these countries.