Alătură-te comunității noastre!

Vezi cele mai recente știri & informații din piața de capital

The selection of shares on the basis of certain factors has become popular again recently. This is nothing new. Even back in the 1990s, numerous publications were describing shares with specific features that defied the teachings of modern portfolio theory (as developed by Markovitz in 1952). This theory suggests that the trade-off of better performance is a higher risk. Reality has frequently contradicted this theory.

So, what are those features that promise a better performance even when adjusted for risk? Dozens of criteria have been analysed and introduced, but to date only a few have been generally accepted:

Equity factors / equity strategies

• Value strategy – Shares are selected on the basis of valuation ratios (e.g. low price/earnings ratio or high dividend yield)

• Momentum strategy – Shares that have beaten the market performance in the past six to twelve months

• Size strategy – Shares with low market capitalisation, i.e. so-called small caps

• Quality share strategy – Shares from companies with highly profitable business models, low gearing, and stable earnings development

• MinVola strategy – Shares with low volatility in comparison with the equity index

In a wider sense, shares from emerging markets can also be regarded as factor strategy, as can growth strategies. That being said, to date there is still no standardised definition for growth as factor. Sometimes past earnings are used for portfolio composition, sometimes future expected earnings, sometimes the price momentum, and sometimes a key ratio like (a high) price/book value.

A possible outperformance of the overall market is one thing, but what about the risk?

Especially in turbulent times on the stock market, many investors feel the need for safety. One measure of safety is volatility. The lower an investment’s volatility, the less painful should the losses be during difficult phases. When the overall market is falling, this affects almost all shares, but possibly at very different degrees.

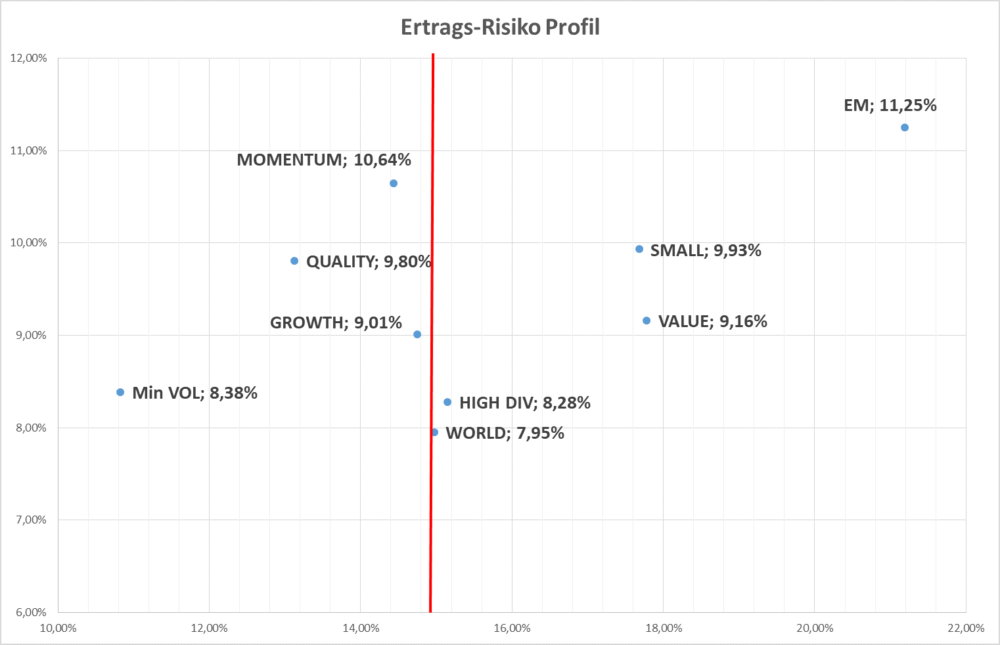

With respect to the most well-known factors, the following chart illustrates the risk (x axis)/return (y axis) profile of the past 20 years:

Source: Bloomberg; Erste Asset Management

All the aforementioned equity strategies (i.e. factors) managed to outperform the market over the past 20 years, albeit not necessarily at the same time. Factor performance is the performance of a portfolio of shares that share one of the above-cited features. The risk associated with the factors, momentum, quality, growth, and MinVola is lower than for the overall market.

Quality shares preferable during turbulent times

High dividends, value, small caps and emerging markets also outperformed the overall market, but at higher risk levels. However, it is during turbulent times in particular when lower risk is a welcome feature. This means that investors should currently focus on quality shares, growth shares, and shares with low volatility. Shares with above-par levels of risk will probably incur higher losses amid market corrections.

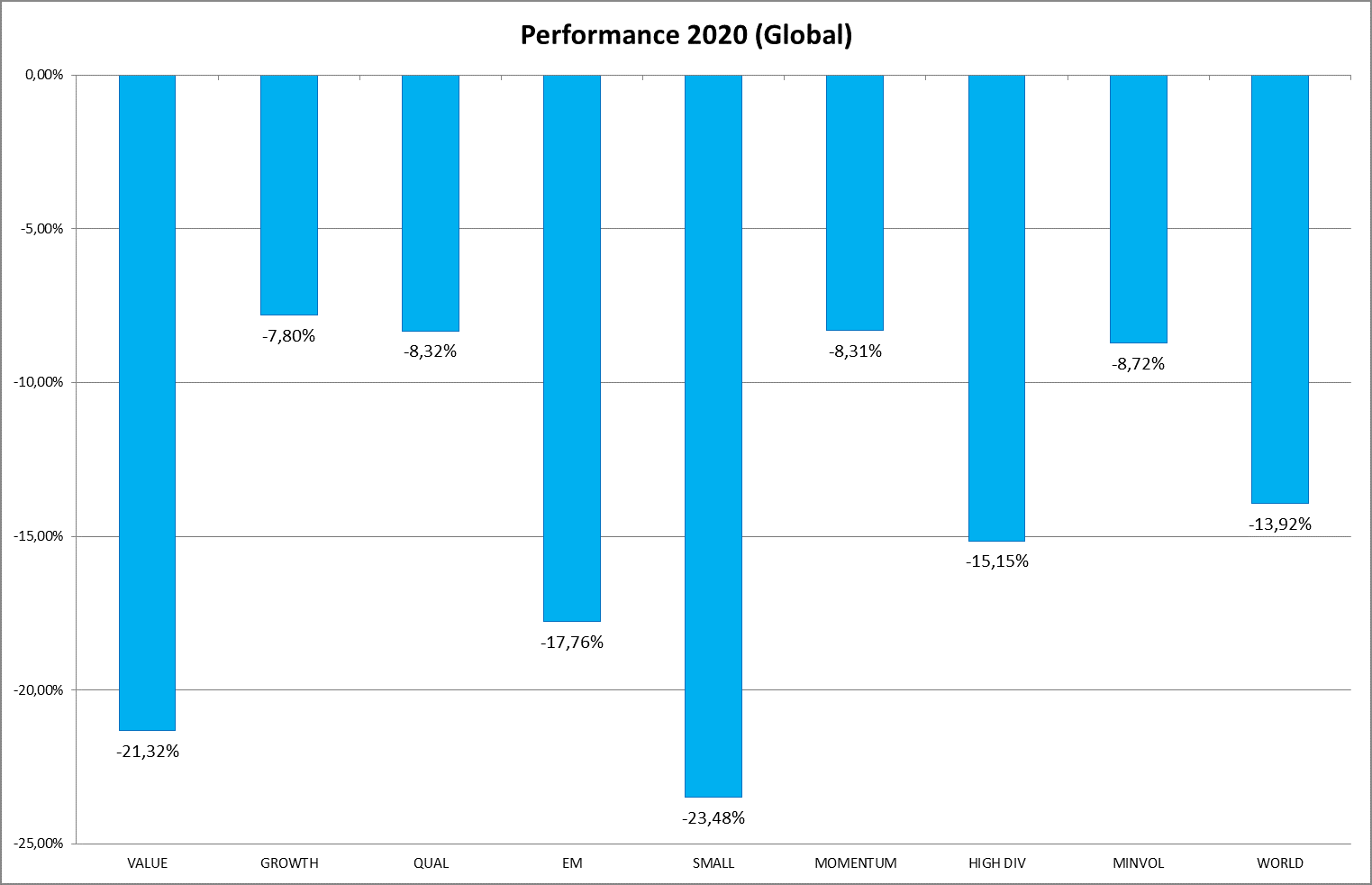

Value small caps, and emerging markets with heavy losses during the crisis

The stock market is currently correcting. From 20 February to 24 March, a global equity portfolio would have lost more than 30% of its value (but would have managed to rebound in the following 20 days by 28%).

The reaction of the various factors discussed above has been rather mixed, as the chart below illustrates. Value shares and small caps have incurred significant losses, whereas quality, growth, momentum, and MinVola shares have fared better. This confirms the gist of chart no.1, according to which some factors are less risky than others.

Source: Bloomberg

In addition to value shares and small caps, shares from the emerging markets were also among the losers, as was to be expected. While value shares tend to command low valuation metrics (e.g. price/book value, price/earnings), this often comes with a reason and does not offer any protection against above-average losses.

These shares depend more significantly on the economic activity and perform badly in the event of a deteriorating economic environment. This means that investors who expect a quick recovery after the corona crisis can now buy value shares at attractive valuations. However, at this point, only a minority still expects a V-shaped recovery.

Quality shares interesting for longer investment horizons

Investors who expect a difficult phase at the stock exchange but who still want to maintain their chances of outperforming the overall equity market will now opt for quality shares with above-average profit growth and low volatility. These shares are particularly well suited for investors with a long investment horizon and for those who do not constantly want to adjust their portfolios to the economic development.

With the courtesy of Erste Asset Management as copyright owner

[ajax_load_more]